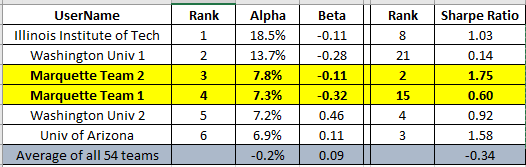

Both of Marquette’s AIM Program teams entered in this year’s Chicago Quantitative Alliance (CQA) Challenge have strong results

The two Marquette AIM program CQA teams rank near the top of all schools participating in this year's Challenge. The contest ends on Friday, March 31, 2017.

|

| Marquette Teams Rank 3rd and 4th based on Alpha generated |

Each year the Chicago Quantitative Alliance (CQA) holds a portfolio management contest for university students, where the students must manage a portfolio with strict requirements. The contest runs each year from the end of October until the end of March.

The CQA is a professional investment organization comprised of leading quantitative investment practitioners. CQA membership includes investment managers, academics, plan sponsors, consultants, and other investment professionals. The primary goal of the organization is to facilitate the interchange of ideas between quantitative professionals.

The CQA Investment Challenge is an equity portfolio management competition that offers students the opportunity to learn and apply stock selection and portfolio management skills in a simulated, real life hedge fund experience. The Challenge provides teams with first-hand experience of being a portfolio manager by managing money, explaining their investment process and discussing performance.

This year Marquette’s AIM Program has entered two teams – one comprised of seniors and the other made up of juniors. The teams, operating under the guidance of Mr. Bill Walker, handle all aspects of portfolio management including stock selection, portfolio construction, and risk management. In addition, each team is required to complete a video presentation at the end of the challenge that provides a review of their investment team, investment philosophy/process as well as an update on performance.

Team members include: Marquette Team 1 (shown below: Brian Shank, Joseph Amoroso, Tim Milani, and Chengbin (Henry) Lu. View the team's YouTube video.

Team members include: Marquette Team 2 (shown below: James Hannack, Connor Konicke, Jack Gorski, Jordan Luczaj, William Reckamp). View the team's YouTube video.

|

| Marquette CQA Team 1 |

Team members include: Marquette Team 2 (shown below: James Hannack, Connor Konicke, Jack Gorski, Jordan Luczaj, William Reckamp). View the team's YouTube video.

|

| Marquette CQA Team 2 |

Throughout the competition teams will work with an assigned CQA member who will serve as a mentor and guide. The Challenge is an invaluable real-life view into managing money in the investment management industry. The Challenge, which is in its 5th year, has had four very successful years with top universities from around the world competing in the event.

The students are tasked with creating portfolios on StockTrak. To learn more about this contest and read what past participants have thought of the contest, please visit www.cqa.org/investment_challenge.

The objective of the competition is to successfully manage an equity long/short market neutral portfolio over the course of the academic year. Key aspects of the competition include:

• The contest runs from the end of October through the end of March

• One team per university. A team can consist of undergraduate junior/senior and/or MBA students. Typically between 3 to 5 members per team.

• A faculty professor will be responsible for selecting and guiding the team.

• Each team will have a CQA member serving as a mentor and advisor.

• The contest will utilize the Stock-Trak investment simulation platform

• The winning team will be determined by the combination of their absolute return, risk adjusted return and an evaluation of a strategy presentation with an emphasis on the risk adjusted returns.

• Prizes will include $3,000 in prize money distributed across the top three teams ($1500, $1000, $500), winning team professor invited to attend the annual CQA fall conference in Chicago (September) or Las Vegas (April) and resumes of winning team students circulated to all CQA members.

When creating the portfolios, the students have to follow certain rules:

· The portfolio has to have a beta of +/- 0.5.

· The portfolio has to be long/short and market neutral.

· The ‘universe’ of potential stocks is limited to 1,000 liquid large and midcap stocks.

· The portfolio has to have less than 5% of its holdings in cash.