|

![]()

|

![]()

JAZZ

Pharmaceuticals PLC. (JAZZ, $156.62): “Listen to the Music!”

By: Danny

Scelza, AIM Student at Marquette University

Disclosure:

The AIM International Equity Fund currently holds this position. This article

was written by myself, and it expresses my own opinions. I am not receiving

compensation for it and I have no business relationship with any company whose

stock is mentioned in this article.

Summary:

• Jazz Pharmaceuticals. (NASDAQ: JAZZ) is a global pharmaceutical

company that focuses on the identification, development, and commercialization

of pharmaceutical products. Their products are centered around medicines for

both adults and adolescents in the areas of neuroscience, oncology, and other.

JAZZ has developed staple brands like Xyrem and Xywav, as well as newly

approved drugs and therapies along with an extensive pipeline of 17 drugs and

therapies in clinical trial phases.

• In Quarter 1 of 2022, JAZZ

reported an EPS of $3.73, lower than the consensus EPS of $3.84 for the

quarter. EPS is up 7% YTD from Q1 2021.

• JAZZ’s vision 2025 plan to

reach a net leverage ratio of 3.5x by the end of 2022, a main point of focus in

JAZZ’s pitch in February, is on pace to meet the goal. Since the close of the

large GW acquisition in Q2 2021, JAZZ has consistently lowered net leverage

quarter-to-quarter and currently have a net-leverage ratio of 3.9x.

Key

points: JAZZ’s recent earnings call showed the company slightly missed

adjusted EPS by $0.11, but the company raised revenue guidance for fiscal year

2022 from $3.5 billion to $3.7. Focusing on Epidiolex, the adopted drug from

the GW acquisition with massive potential, product sales YTD are up 6.7% and

accomplished $18 million inventory build in 2021 Q4, majority reserved for this

past quarter. Commercialization of Epidiolex in European markets continues on

pace with the drug fully available in 4 of 5 key European markets with an

expected launch in France by the end of this year.

Recently launched and near-term R&D pipeline opportunities remain promising with the addition of two new early-stage molecules. Programs emerging from the cannabidiol platform are on track to begin additional phase 3 trial for Epidiolex in epilepsy later this quarter, which could bolster this drugs outlook. Ongoing compelling Xywav clinical trials to address idiopathic hypersomnia remain strong following the first full quarter of treatment options for IH that don’t just address symptoms. Active patients taking Xywav for IH has grown 200% over the past quarter.

Earlier this quarter, JAZZ acquired global development and commercialization rights to Werewolf Therapeutic’s WTX-613, worth up to $1.2 billion. "We believe WTX-613 has the potential to minimize the toxicity associated with systemic IFNα therapy, preferentially delivering IFNα to tumors, and thereby expanding its clinical utility in treating cancer," said Rob Iannone, executive vice president, global head of R&D of Jazz Pharmaceuticals. JAZZ made an upfront payment of $15 million, and Werewolf is eligible to receive a tiered, mid-single-digit percentage royalty on net sales of WTX-613.

What

has the stock done lately?

After

beating EPS estimates of $3.64 by producing a 2021 Q4 EPS of $4.21, JAZZ’s

stock price rose 12% and continued to trend positively reaching a six-month

high of $168.66. After their recent missed earnings, the stock dropped 4.7%. Focusing

on organic growth and taking a back seat on more major investments following

the GW acquisition, the company has seen their new top line drivers gain

traction as they lower their net leverage ratio, making recent stock price drop

nothing catastrophic to its long-term outlook.

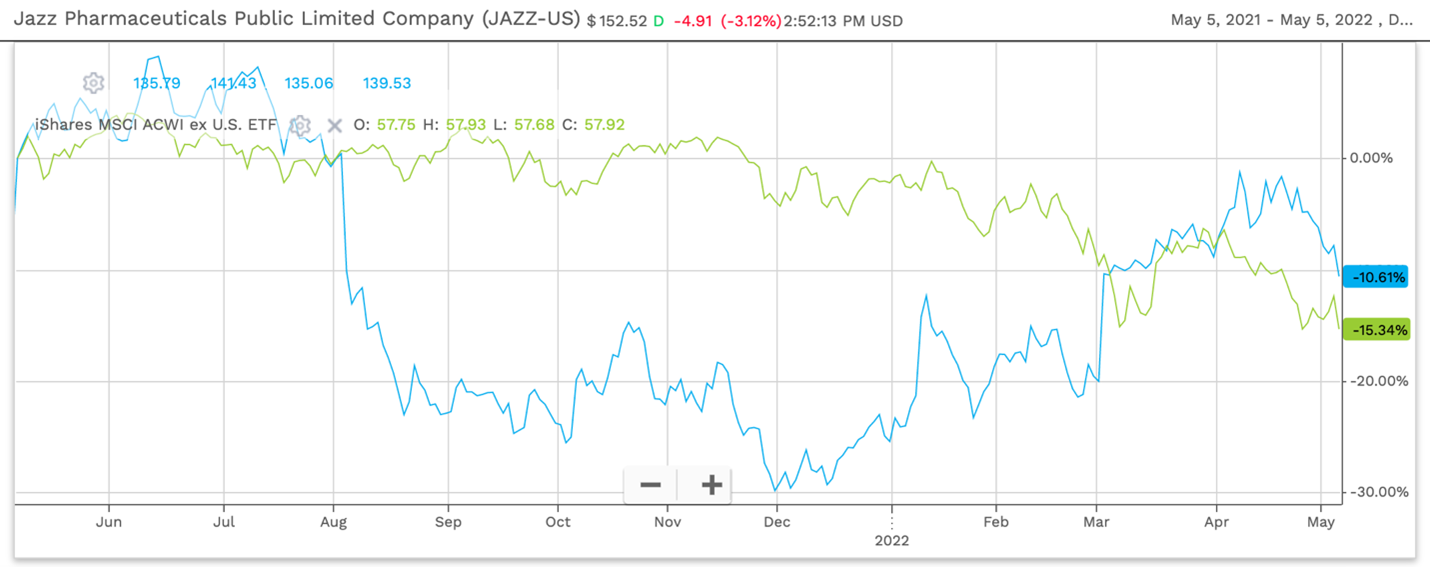

Past

Year Performance: In the last year, JAZZ is down 11.68%, with a

high $181.17 and a low price of $122.41. The iShares MSCI ACWI is down 8.28%

over that same time. The low-price period was due to the expected aftermath of

the GW acquisition which caused JAZZ unprofitability for quarter’s 2 3 and 4 of

2021.

My

Takeaway

Following the recent earnings

report, the stock price declined due to missed EPS guidance, but revenue outlook

for the year increased by $200 million. When AIM international fund acquired

JAZZ, their expanding drug portfolio and robust pipeline was essential to

driving top line growth and overall company growth. Financial goals and

continued guidance remain consistent with initial outlook presented, making the

long-term outlook on JAZZ strong. As top line growth and drug specific market

penetration continues, JAZZ is a strong recommended HOLD.

Casey’s

General Stores (CASY, $201.30): “Pizza and Gas, an

Unlikely Combination”

By: Max

Tiemann, AIM Student at Marquette University

Disclosure:

The AIM Small-Cap Equity Fund currently holds this position. This article was

written by myself, and it expresses my own opinions. I am not receiving

compensation for it, and I have no business relationship with any company whose

stock is mentioned in this article.

Summary

Key

points: Ever since Darren Rebelez took over

as CEO, Casey’s has aimed to have 8-10% EBITDA growth year over year. This

growth is needed due to the revenue lost from the Covid-19 pandemic. To achieve

this high growth the company has implemented a variety of strategy to

ultimately increase earnings for shareholders.

The first

growth strategy that Casey’s has implemented is store growth and acquisitions.

Since 2010, the company has increased stores by a 4.37% CAGR and currently

operates over 2,458 stores. Casey’s increases their stores by either new store

builds or through acquisitions. This past year the company acquired 178 stores

from other gas stations.

The

next growth strategy that Casey’s has implemented is partnering with UberEats

and DoorDash. This partnership allows the company to earn revenue from digital

orders and ultimately target a different customer base.

Another

growth strategy that Casey’s has implemented is introducing a digital app and

their own brand. With over 4.2 million people on the Casey’s app, the company has

been able to earn revenue from digital sales of grocery and prepared foods. On

top of that Casey’s introduced their own brand that allows them to increase

their gross margin by having a lower cost of goods sold on their branded foods.

By combining

all these strategies, Casey’s aims to earn 8-10% EBITDA growth over the coming

years.

What

has the stock done lately?

Over

the past six months, CASY is up 4.39%. This increase can be attributed to management’s

growth strategy of acquisitions and adding more stores to increase earnings. Over

the past month, CASY is up 0.61% but over the past five days the stock is down

4.52%. This displays that recently CASY has had success and their returns may

be skewed from a difficult week.

Past

Year Performance: Over the past year, CASY is down 9.74%. However,

this decrease primarily came in the beginning of the year. Over the past six

months CASY is up 4.39%, displaying that management’s growth strategy has been

effective in increasing earnings and the share price.

My

Takeaway

I believe that Casey’s General

Stores growth strategy will prove to be successful. By combining the strategies

of unit growth, digital sales, and their own brand, I think the company will be

able to grow their EBITDA and ultimately increase EPS. On top of that, I think

the Covid-19 pandemic forced Casey’s to miss out on a ton of foot traffic which

ultimately decreased revenue and their share price. As the world finally

returns to normalcy, I believe the stock price should continue to increase.

STMicroelectronics NV ADR RegS (STM, $37.64): “ST(MEMS)”

By: Kevin

Igoe, AIM Student at Marquette University

Disclosure:

The AIM International Equity Fund currently holds this position. This article

was written by myself, and it expresses my own opinions. I am not receiving

compensation for it, and I have no business relationship with any company whose

stock is mentioned in this article.

Summary

Key

points: STM through Q1 2022 has earned designed wins with

their power modules and module maker using Gen3 SiC MOSFET technology EV Traction

Inverter applications. What this

technology does is help eliminate tail current during switching which results

in faster operation, reduced switching loss, and increased stabilization. Along with this effective use of new

technology STM has also designed their next-generation stellar automotive MCU

into a new zonal architecture for software-defined vehicles.

In STM’s latest earnings presentation

they explained for their industrial segment they ranked number one worldwide in

general purpose microcontrollers for 2021.

While also introducing their first intelligent sensor processing unit

with Gen3 MEMS. MEMS is a process

technology used to create tiny integrated devices or systems that combine mechanical

and electrical components helping their products become more efficient and in

return attractive to customers. Finally, STM has grown their sockets in various

industrial applications helping them target the growing markets of renewable

energy and power saving technologies.

STM has planned to invest about

$3.4 to $3.6 billion in CAPEX to increase the production capacity and strategic

initiatives. The first of their investments

being in their new industrialization line located in Italy. Based on the strong demand from customers and

planned future investments STM has a goal of revenues for 2022 to be in the

range from $14 billion to $15 billion.

This target goal would mean a growth of about 17%. After quarter one 2022 they have done $3.55

billion in revenue currently being on track with their projected growth for the

current year.

What

has the stock done lately?

In the past week STM has seen an

increase of 3.32% after releasing earnings for quarter one fiscal year 2022 on

April 27th. The company

reported EPS of $0.79 and revenue of $3.55 billion beating estimates in both

categories. This could be the momentum

boost the companies needed after decreasing 11.79% in the past month.

Past

Year Performance:

STM year to date has decreased 25.02%. This has been closely related to the current semiconductor shortage that has been going on for the last year and a half. The reduction in car sales has also impacted STM’s automotive segment operations.

My

Takeaway

I believe STM is well suited for

the future with the semiconductor industry taking a large impact from

implications relating to the Covid-19 pandemic.

Research has shown that the global semiconductor should grow about 10% through

the end of 2022 proving there is growth opportunities for STM to potentially

capitalize on. With their impressive revenue

in quarter one staying on track with management’s plan to reach about $14

billion in total revenue for 2022 and advancements being made in the automotive

and industrial industries I believe STM has tremendous opportunities for

growth.

National Vision Holdings, Inc. (EYE, $38.97)

By:

Grace McCrea, AIM Student at Marquette University

Disclosure: The AIM

Small-Cap Equity Fund currently holds this position. This

article was written by myself, and it expresses my own opinions. I am not

receiving compensation for it, and I have no business relationship with any

company whose stock is mentioned in this article.

Summary

● National

Vision Holdings, Inc. (NYSE: EYE) specializes in the

sale of optical products, specifically eye care and eyewear. The majority (91%)

of revenue is generated from the Owned & Host segment, which contains sales

from the eyeglass companies that EYE works with. The remaining revenue comes

from the Legacy segment, which processes

inventory and lab services.

● Just a few weeks ago, on April 11,

2022, EYE added Joe VanDette to their company as Chief Marketing Officer. He

has previous experience at Smart & Final (grocery), as well as at Toys ‘R

Us (clothing and toy retailer) in positions involving marketing, analytics, and

strategy.

● In an investor presentation released in

March 2022, EYE emphasized that their store count has been increasing at a CAGR

of 7% for 16 years. Although their new store success rate is a very impressive

97%, a comment about their commitment to e-commerce would have been beneficial.

In order to accommodate younger generations who prefer online shopping, it will

be necessary for EYE to focus on improving their experiential platform in the

digital space.

Key Points: Although

EYE has been committed to Corporate Social Responsibility (CSR) for over 30

years, they began a special dedication to CSR in 2021, which started with an

Impact Report. In order to evaluate their historical commitment to CSR, EYE

organized a strategic assessment and a sustainability assessment.

To

begin these assessments, EYE identified their most prevalent environmental

impact locations throughout the business. This helped clarify focus areas of

CSR that need improvement at National Vision Holdings. Finally, management

created a governance structure, lived out in the Board of Directors, to

prioritize CSR initiatives.

In

addition to this commitment towards CSR, EYE has an advantage in the market as

a whole, which is important for their future success. According to management,

EYE currently has 965 locations throughout the country, which only represents

about 31% of the total available market. The other 69% of the market represents

extreme growth potential for National Vision Holdings, Inc.

What has the stock

done lately?

The

overall markets saw a rough start to 2022, and recent macroeconomic issues like

the conflict between Russia and Ukraine have not helped. However, in their

Q4FY21 earnings call on Feb 28, 2022, EYE reported a 4.46% increase in revenue,

signifying that they beat earnings. This is significant for many reasons, but

primarily because it marks the first year that EYE brought in net revenues

greater than $2 billion. Even with this positive news, EYE has reported a YTD

return of -21.57%. This is likely due the company’s struggle to report

pre-pandemic same store sales growth.

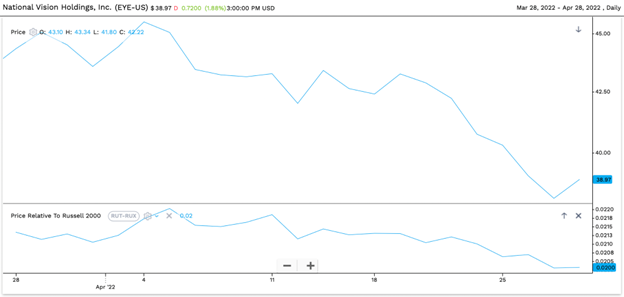

Past Year Performance: EYE’s

performance over the past year has been quite volatile, resulting in a 52-week

return of -26.47%. As shown below, as of April 28, 2022, the stock is rather

cheap and trading near its 52-week low of $34.70.

My Takeaway

EYE’s

dedication to CSR is impressive. Commitment to corporate social responsibility

and/or environmental social governance is currently a majority of investor's

priority and preference. It’s really important to know what investors, as well

as customers, want. With this in mind, I would like to see a stronger

commitment to their customers through e-commerce. With one of their closest

competitors being Warby Parker, who is known for offering an exceptional online

experience for “trying on” glasses, EYE must commit to the younger generations

who prefer to shop this way.

Eaton

Corp. Plc (ETN, $145.71): “The (electrical) Power of Eaton”

By: Zach

Turbett, AIM Student at Marquette University

Disclosure:

The AIM International Equity Fund currently holds this position. This article

was written by myself, and it expresses my own opinions. I am not receiving

compensation for it, and I have no business relationship with any company whose

stock is mentioned in this article.

Summary

Key

points: Late last year, Eaton completed the

sale of its hydraulic business to Danfoss (a danish industrial company) for

$3.3 billion. The hydraulic business was seen as a large but

slower-growth, lower margin business than the rest of the company. With the

sale of the hydraulic business, it marks as another milestone for the company’s

transformation into a higher growth company. Additionally, this sale will

provide great value for its shareholders as it earns higher returns.

Eaton completed a very recent

acquisition of Royal Power Solutions which will synergize well with its already

existing electrical segment. With Eaton’s continued commitment to improve

quality of life through power management technologies, this will allow the

company to excel. Also, this acquisition will give them the ability to

capitalize on their fast-growing eMobility, Aerospace, and electrical

businesses.

In the past year, the world has

experienced major setbacks due to the pandemic, supply chain constraints, and

rising inflation. Throughout this period, ETN has continued to show financial

strength. For FY 21’, sales were up $19.6 billion dollars, representing 10%

organic growth. In fact, all segment margins were up 18.9% which was an all-time

record for the company. Additionally, the company continued to reinvest in the

already growing company with $575 million going towards Capex and $616 million

towards R&D activities. Lastly, Eaton returned $1.2 billion to their

investors through dividends, and through this same period, their share price

grew 44%.

What

has the stock done lately?

As of late, the stock has seen

increased volatility since the beginning of this year. At the beginning of this

year, ETN’s share price was $170.56, and today it sits at $145.71, representing

a decrease of 14.5%. This decline in price is partly due to the current

geo-political tension between Russia and Ukraine, and ongoing supply chain

constraints.

Past

Year Performance:

ETN’s 52-week range stretches from $139.12-175.72, with its

low trailing back to mid-June of last year. Today, the share price is hovering

very close to its price of that a year ago. In August of 2021, ETN saw a slight

dip from $168.84 to $148.39 due to the CEO’s press conferencing speaking on the

supply chain issues. He explained that the company will have challenges when

respect to their revenue. However, the share price quickly bounced back in the

following months hitting its all-time high. The company will be releasing its

Q1 2022 earnings on May 3rd.

1 Year Stock Chart vs. Benchmark from FactSet here

My

Takeaway

ETN was added to the portfolio at

the end of 2018 and has seen extraordinary growth since then. Although the

company has seen many macro-economic challenges, ETN has stayed strong and has

continued to push forward. Also the company has continued to be a pioneer in

power solutions with its high M&A activity, key customer wins, and many

development programs. Moreover, ETN is joined Bill Gates’ Breakthrough Energy

Ventures and the UK-based Business Growth Fund in providing venture capital

support to Reactive Technologies. The company still faces headwinds with the

ongoing supply chain crisis in which they will need to effectively manage. With

the company’s strong performance prior to the war between Russia and Ukraine,

there is no doubt that Eaton will be a strong performer in the industry and

compared to its peers.

1 Month Stock Chart from FactSet here