By:

Nathan Zirpolo, AIM Student at Marquette University

Disclosure:

The AIM Equity Fund currently holds this position. This article was written by

myself, and it expresses my own opinions. I am not receiving compensation for

it and I have no business relationship with any company whose stock is

mentioned in this article.

Summary

• Dana Incorporated (NYSE:DAN) is a global provider of automobile

parts for cars ranging from golf carts to bulldozers. The company operates in

four segments, Light Vehicle, Commercial, Off-Highway and Power

Technologies.

• Dana’s Q3 net profit

increased 16.8% QoQ form $95m to $111m.

• The company has seen 12

consecutive quarters of year-over-year sales growth.

• Management believes

that the recent acquisition of Nordresa gives the company a direct relationship

with the OEM of their customers, creating less costs in their supply chain.

• With a recent stock

price surge due to a strong third quarter performance, Dana could be heading to

new 52-week.

Key

points:

When managing a sector that has outperformed the

portfolio over the prior years, there are more eyes looking over the seven to

ten names, looking for any news either sell or hold the companies. With a

general understanding that an economic slowdown is approaching, the Consumer

Discretionary sector’s returns could swing in the other direction due the

sectors returns being positively correlated a strong market. While Dana has increased

over 30% since the company was purchased in early October, the stock still

remains ‘in-play’.

Over the past year, the

company has completed acquisitions to increase their position in the electric

vehicle market. While they have supplied EV auto parts for high end cars, the

company does not believe they can be as profitable in the passenger car

business as they could with providing parts for other types of vehicles that

are covered in other segments. This was a main driver when pitched, and despite

the recent stock surge, this driver has not been played out and is not priced

into the stock price.

Over the past month, Telsa

has released their version of a pick-up truck while Ford released their version

of an all-electric Mustang. With over 200k Cybertrucks already preordered, the

shift to electric vehicles is larger than it has ever been before, creating

business opportunities for Dana, who can provide a wide range of electric auto

parts to a wide range of vehicles, as mentioned above.

In the past month, hedge

funds and other institutional investors have increase their holdings of DAN,

showing that the general sentiment in the market believes that the company will

prosper into the future.

What

has the stock done lately?

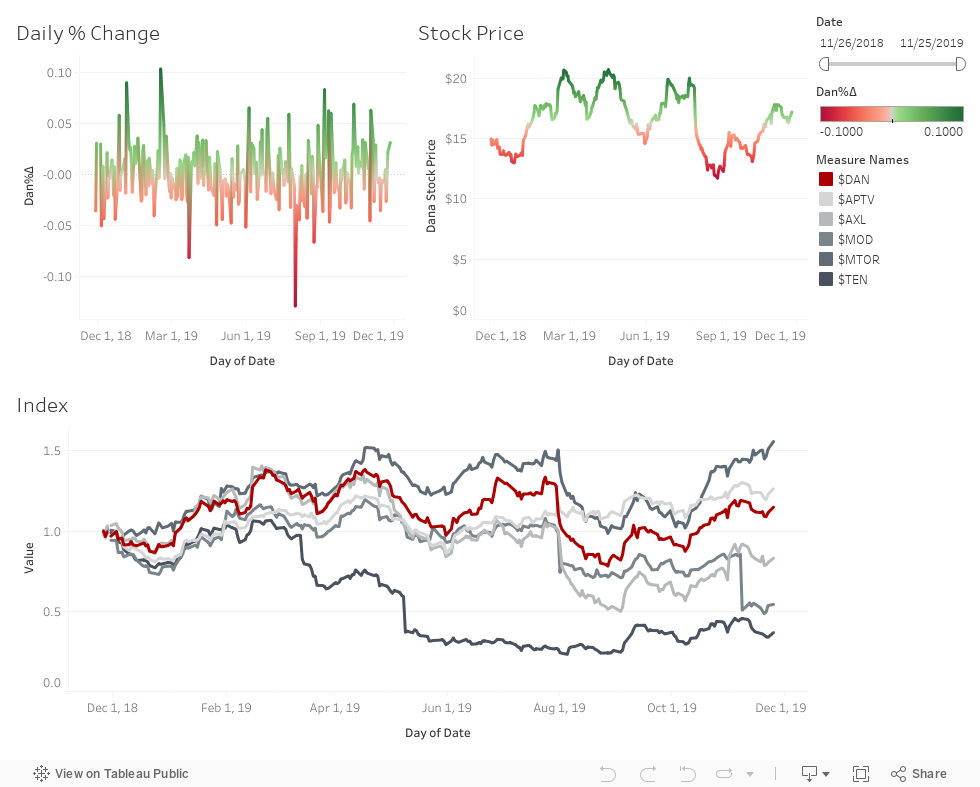

Since acquiring this

company in early October at $13.51, the firm has soared over 31% 5 in the past

quarter, and currently sits at $16.69. When comparing this increase to the

S&P 500 Index which increased 7.2% in the third quarter, Dana has increased

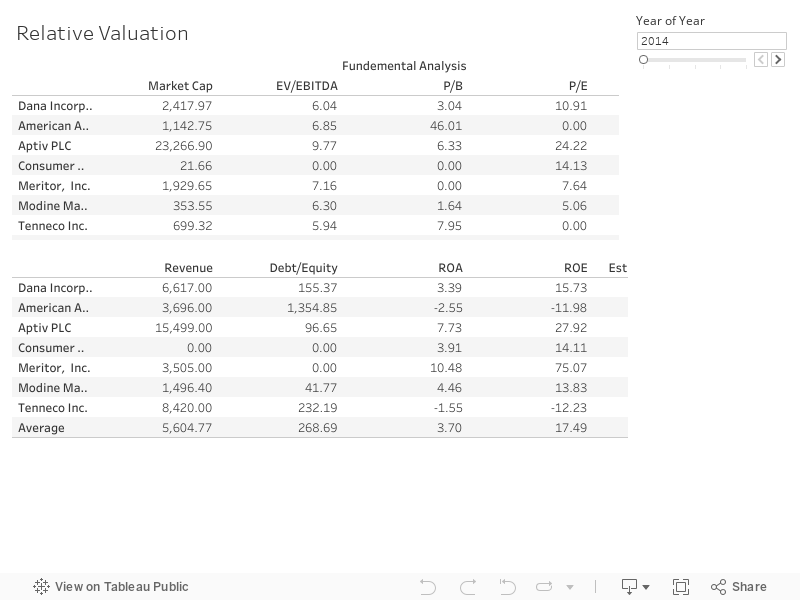

23.9% relative to the index during this time. The company is trading 0.9 times

more in the third quarter.

Past

Year Performance:

Dana has increased just over 10% over the

last year, however this can show that the AIM program purchased the company

near their floor, implying that there is still more room to grow. The company

saw a 52 week low of $11.57 in mid-August, slowing rallying to their current

price of $16.69. While Dana has seen a price increase of over 30% since pitched

just two months ago, there should no reason for concern that the stock will

return to the prices seen in August.

My Takeaway

Due to Dana’s stock price

surge paired with strong third quarter numbers, the current holding of Dana

should not be questioned, and should continue to be held by the program. After

reviewing the original pitch, the three drivers listed have affected the stock

price, thus not being priced in. The AIM program should continue to hold DAN as

they grow their EV segment.