By:

Danny Smerz, AIM Student at Marquette University

Disclosure:

The AIM Equity Fund currently holds this position. This article was written by

myself, and it expresses my own opinions. I am not receiving compensation for

it and I have no business relationship with any company whose stock is

mentioned in this article.

Summary:

• Toronto Dominion Bank (NYSE:TD) engages in providing financial

products and services. It operates in the following business segments: Canadian

Retail, U.S. Retail, and Wholesale Banking.

• In 2018 Q4, Net

Interest Income was up 9% in the Canadian Retail Segment of the business (57.7%

of Total Geographical Revenue).

• Total Deposits are up

to $851.4B in FY 2018 compared to $832.8 B in FY 2017.

• Dividend payouts increased

11% on a full-year basis.

• Recently announced a

long-term agreement with Air Canada to become their primary credit card issuer

(takes effect in 2020).

Key

points:

Toronto Dominion Bank remains solid as we move

forward. Both the Canadian and U.S. economies remain in a strong position as we

enter 2019. On a macro scale, it can be expected that the company will

experience further margin expansion given the rising interest rates and

positive credit quality.

The Canadian Retail

Business segment experienced 10% earnings growth over FY 2018. This increase

was largely driven by higher levels of customer acquisition/retention and

growth in business loans and deposits. The U.S. Retail Bank segment experienced

even higher earnings which rose 23% over the past year. The favorable

environment in the U.S. over the past year goes in hand with the benefits

conferred by higher rates and U.S. tax reform.

Pressing forward, the

Canadian Bank has made it clear that they’re at the forefront of customer

experience. They’ve gained recognition for their digital banking app—earning

the top spot in Canada according to App Annie. Furthermore, their recent

partnership with Roostify, a digital lending platform provider, will mitigate

the hassle and issues for those applying for a mortgage. Overall, this will

help to enhance and expand their customer base.

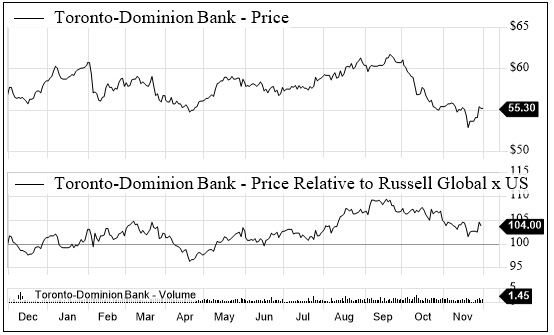

What

has the stock done lately?

Over the last month the

stock has traded between $55.55 and $55.30. During this time the stock reached

a low of $52.92 on November 20th. This is the lowest trading price

of the stock in the past year. Since then, the stock is up ~4.5%. This increase

is driven by the recent announcement of estimated annual reinvested

distributions for TD ETFs as well as entering into a long-term agreement with

Air Canada.

Past

Year Performance:

TD Bank has decreased

2.47% in value over the past year. However, the stock is coming off a one-year

low. Considering their YOY Net Interest Margin and dividend growth, this might

be the right time to buy more.

Source:

FactSet

My

Takeaway:

Toronto Dominion Bank’s

stock performance is heavily dependent on interest rates and efficiency

improvements. The bank currently has an efficiency ratio of 55%--demonstrating

that resources aren’t being converted into revenue as often as they possibly

could. Nonetheless, their improvements and partnerships within their digital

platform is a winning approach with customers. Increasing interest rates on the

horizon for both Canada and the U.S. will continue to drive top-line growth.

Source:

FactSet

Sources:

FactSet

FactSet

Toronto-Dominion Bank (2018). Q4

Earnings Call Transcript.

Retrieved from FactSet online database.