By: Philip Suess, AIM student at Marquette

University

Disclosure: The AIM Equity

Fund currently holds this position. This article was written by myself, and it

expresses my own opinions. I am not receiving compensation for it and I have no

business relationship with any company whose stock is mentioned in this

article.

Summary

(This is an example, you would add your own content below)

•

LendingTree, Inc. (NASDAQ: TREE) is

an online platform which promotes lending by matching consumers with various

lenders and providing consumers with the necessary tools to evaluate different loan

offers. Their revenue is split between mortgage products and non-mortgage

products such as credit cards, personal loans, small business loans, and

student loans.

•

The rising interest rate environment poses a risk to demand for mortgage and

nonmortgage loans as the cost of borrowing increases.

•

Signs of inflation and market correction suggest the economy is late in the

business cycle which is worrisome as LendingTree operates in a very cyclical

industry.

•

LendingTree currently has over a million exercisable stock options outstanding

expected to be exercised this year which will likely be dilutive despite

expected share repurchases.

•

Looking forward, LendingTree’s rapid revenue growth is expected to slow and

increases in shares outstanding will likely cause the stock price to begin moving

down.

Key points: In his February testimony before Congress,

Chair Powell reiterated his expectation of several rate increases from 2018

through 2019. These expected rate increases will push up the historical low

borrowing costs decreasing the demand for loans. Lending Tree derives 55% of

revenue from non-mortgage products and 45% from mortgages. Both of these

segments could experience a slowdown in growth resulting from higher interest

rates.

January’s

wage inflation number of 2.9% is the first sign of a needed wage in several

years. This number is a positive sign for the economy but has some worried that

the economy is going to experience too much inflation. Experiencing too much

inflation would result in significantly higher prices and may ultimately lead

to a slowdown in economic growth. LendingTree would be harmed by this change in

the business cycle as their business is very cyclical given the nature of

lending.

Stock

options are a significant risk to shareholder value as there currently over a

million exercisable options outstanding and only 12.25 million shares

outstanding. A majority of these options are held by the company’s CEO, Douglas

Lebda and will expire in 2018 if not exercised. Management stated it will

attempt to address this risk by increasing share repurchases but it acknowledge

that they will likely be unable to purchase enough shares to eliminate the

dilutive effect. Currently, CEO Lebda is the second largest shareholder owning

12.93% of shares outstanding.

What has the stock done

lately?

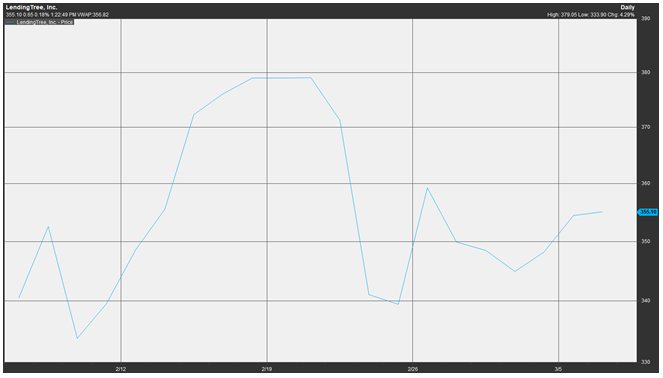

On

February 22, LendingTree reported earnings of $0.84 missing consensus estimates

by $0.06. Following the earnings miss, the price dipped from over $380 down to

$340. Since the reporting date, the stock has been trading between $340 and

$360. This recent decrease in response to the earnings call as well as a

decrease from over $400 to $365 during January’s market correction suggest the

stock’s historic run may be coming to an end.

Past Year Performance: Over the past 12 months, LendingTree’s

share price increased by 202%. Moving forward, management may have trouble

meeting their growth projections given the changing macroeconomic environment.

Additionally, exercised share options are expected to outnumber share

repurchases. Given these two risks, it will be very challenging for management

to continue to increase shareholder value in 2018.

Source: FactSet

My Takeaway

The

changing macro climate poses a considerable risk for LendingTree in 2018. Their

business may be negatively impacted from both rising rates and the possible end

of the business cycle. Exercisable stock options are another worry for

shareholders moving forward. Even if the current expansionary period continues

through the end of 2018, pressure from rising rates and additional shares is

expected to keep the stock from returning to January’s share price of $400. Given

these concerns, it is time to uproot and sell the Tree.

Source: FactSet