Cohen & Steers (CNS, $28.25): Steering Clear into 2016

By: Ryan Johnston, AIM Student at

Marquette University

Disclosure: The AIM Equity Fund

currently holds this position. This article was written by myself, and it

expresses my own opinions. I am not receiving compensation for it and I have no

business relationship with any company whose stock is mentioned in this

article.

Summary

•

Cohen & Steers. (CNS) operates

as an investment manager in the United States and internationally. The company

focuses on global real estate securities (REITs), global listed infrastructure,

real assets, large cap value stocks, and preferred securities.

•

Well, it finally happened - the U.S. Federal Reserve moved interest rates up. So what happened with REIT performance? On the day Fed Chair Yellen

announced the increase, the REIT index jumped 2%; but over the last twelve

months the index is down approximately 6%, which is in-line with the S&P

500’s performance. Overall, REIT performance has not been punished because of

solid fundamentals.

•

I had some concerns over Martin Cohen toning down his role at Cohen &

Steers. So far he has remained a visible company and industry leader. While it

sounds like he is enjoying semi-retirement, Bloomberg and The New York Times

have interviewed him on the state of the REIT environment. Mr. Cohen has not

sold any of his 25% approximate stake in the firm, which is always reassuring.

•

Cohen & Steers has conquered REITs, what about real assets? In the firm’s

third quarter conference call, Mr. Steers indicated a large portion of the

firm’s focus would be on real assets. The goal is for the firm to be considered

a master of the real assets space, much like it is with REITs. There is one

huge, real issue blocking their way and that is performance. Real asset

strategies across the board have struggled, leaving investors with very little

incentive to jump on board. If the underlying investments of real asset

strategies begin to rip, I would expect their AUM to quickly follow suit.

Cohen & Steers. (NYSE:CNS) Since initiating coverage on Cohen

& Steers during mid-November 2015, fundamentally not much has changed at

the firm level. The largest change comes from their AUM flows. As of November

30, AUM decreased to approximately $52 billion; this change was expected

because of market conditions. Generally, $600 million in market depreciation

was the leading contributor to the decline, as well as an institutional decline

of almost $100 million, which was offset by retail investors in open-end mutual

funds with an increase of $120 million.

While

the firm does not provide color on the origin of strategy inflows and outflows,

I believe the open-end mutual fund inflows were into preferred securities. Over

the past few quarters, there has been an increase in popularity of Cohen &

Steers’ preferred securities fund because of their high-yielding nature and

increasing coupon rates. While this may sound counter intuitive to an astute

investor, the reason is because a large portion of preferred securities are issued by banks, who stand to benefit from a rising rate environment. Also, a

large portion of preferreds are fixed-to-floating rate securities, meaning as

interest rates rise, so do their coupon payments. This product popularity is

exciting for the firm and may help organically increase AUM over the next few

years so long as rates continue to rise.

Lastly,

going into 2016, I am going to be keeping a close eye on AUM growth,

particularly growth stemming from real asset strategies. If Cohen & Steers

were to experience any real and meaningful growth it would be from this asset

class. Real assets, like REITs, will never be a large allocation of a typical

diversified portfolio, but it does play an important role. That is why if

performance of the underlying investments were to begin to increase, the

popularity of the product will increase as well. Cohen & Steers has

everything in place including a great team, sensible investment philosophy and

process, and leading asset class research, all they are waiting and hoping for

is performance.

What has the stock done lately?

Since

the Domestic AIM fund initiated coverage, the stock has remained in a

relatively tight trading range of $28-$31. Recently the share price has slid

due to weaknesses in global markets. As I have stated before, there has been no

new information disclosed besides what was released in December regarding

November’s AUM. Management has not yet released the date for fourth quarter

earnings.

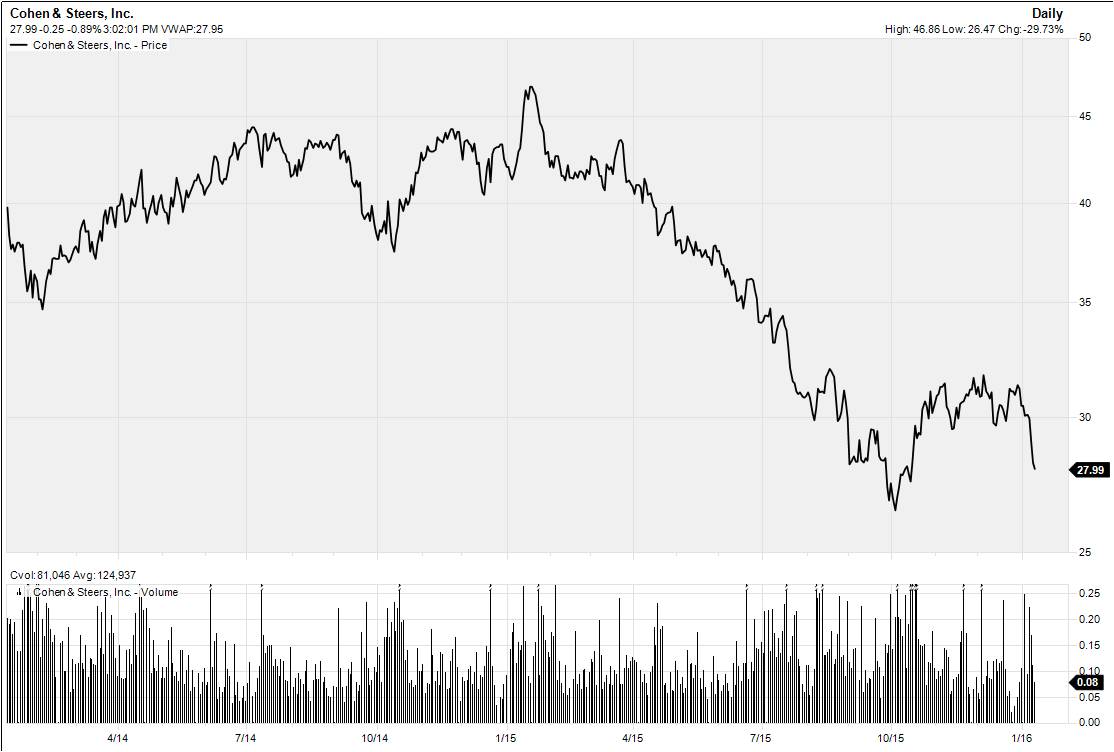

Past Year Performance: Looking back to the beginning of 2015,

the stock had a very rough year with a 33% decline, which after constructing a

DDM and P/E multiple, shows the firm is trading at a 39% discount. Overall, I

believe the share price is depressed because of investors’ knee jerk reactions

that interest rates will negatively affect the company’s fund performance.

Underlying that assumption is the Fed gradually raising interest rates over the

next few years. I believe these assumptions are totally within reason and

should be fully baked into the stock price in the next two to three years.

My Takeaway

As

the monthly chart below shows, while CNS has fallen, this stock's performance is in line with the Russell

2000 during the past four weeks. I would expect the stock to perform above the financial sector benchmark for the remainder of 2016.

As

I see it, this is a simple ‘value with a catalyst’ play. While there are

exciting new and growing products like real asset and preferred security funds,

the stock is simply undervalued to its competitors and historical average. None

of their products have been impaired and have demonstrated relative resilience

during all market cycles. This demonstrates to me that the firm is on a stable

foundation to continue their modest growth trajectory, by offering unique,

industry leading products and having a sticky investor base. Because of aforementioned

catalysts, I believe this stock has a 39% upside, with very little downside due

to the firm’s mature nature in the asset management industry. I strongly

encourage you to read my original

write-up posted on November 13th, which will provide more clarity and

background on my investment thesis and thoughts.

Source: Yahoo Finance