By:

Derek Gross, AIM Student at Marquette University

Disclosure:

The AIM Equity Fund currently holds this position. This article was written by

myself, and it expresses my own opinions. I am not receiving compensation for

it and I have no business relationship with any company whose stock is

mentioned in this article.

Summary

• Novanta Inc. (NASDAQ: NOVT) is a global supplier of technology

solutions to both the healthcare and industrial OEM manufacturers.

• The company reported

earnings on August 6th, meeting consensus EPS estimates on the dot

at $0.54 and slightly beating sales estimates at $155m v. $154m est.

• The share price has

nearly doubled over the last 24 months, fueled by a strong diversification of

business. The Vision segment has seen sales growth of over 90%, while the

Precision Motion segment has grown by over 50%.

• On June 24th,

Novanta announced they would acquire Arges GmbH, a German manufacturer of laser

scanning subsystems used in medical applications, for a purchase price of $37.6

million.

• This stock is at the

far end of the growth spectrum. Novanta has seen sales and net income more than

double since 2012, and its multiples have skyrocketed relative to competitors

and historical averages over the past two years.

Key

points:

Novanta Inc. provides

core technology solutions to manufacturers to medical and advanced technology

equipment manufacturers. The company seeks to innovate what they dub as

“mission critical technologies” to improve factory efficiency and medical

success. The company reported Q2 earnings on August 6th, with

quarterly revenue up 3.2% YoY, but down 1.2% since last quarter. Sales have

been stagnant as of late, with quarterly revenue only up 6.0% over the past 7

quarters. Novanta has proved resilient in the face of a mixed bag of

developments in the macroeconomic landscape. Although medical market spending

saw double digit growth in the second quarter, industrial spending is a

legitimate concern moving forward. The Purchasing Managers Index (PMI) is at

its lowest level since early 2016 amid economic uncertainty. Bookings are

proving hard to come by for the microelectronics segment of Novanta’s sales mix

(10% of revenue). An overall 30% decline in the microelectronics sector with

further declines forecasted by management are not appealing to me as an

investor.

Although I may strike a

pessimistic tone, the stock has performed well since being added to the

portfolio in March of 2018. The share price has nearly doubled over the last

two years, while we have enjoyed a ~53% return. The driving force behind the

share price spike has been the growth of both the Vision and Precision Motion

segments, which have grown over 90% and 50% in the past two years,

respectively. Of the three segments, I expect future growth to come from the Vision

segment, which primarily supplies medical customers. This segment has been less

affected by industrial headwinds and trade concerns, and has experienced

continued success in new product launches (new product revenue YTD increased

75% YoY). I expect this segment to continue to increase its share in the sales

mix. Decreasing bookings and tariff exposure make me skeptical of the Photonics

and Precision Motion segments capability for near-term growth.

In 2019, Novanta has

closed on three acquisitions to bolster their new product offerings, which have

been a source of consistent growth. The purchases of Ingenia for $16.2 million,

Med X Change, Inc. for $21.8 million, and Arges for $37.6 million have been a

significant use of cash and have added to a modest debt load. Arges was by far

the biggest acquisition, with an additional future payment of ~$38 million

likely due in mid-2020. Part of management’s strategy has been to diversify and

decrease exposure to trade sensitive markets through acquisitions, and it looks

like they are executing on this strategy.

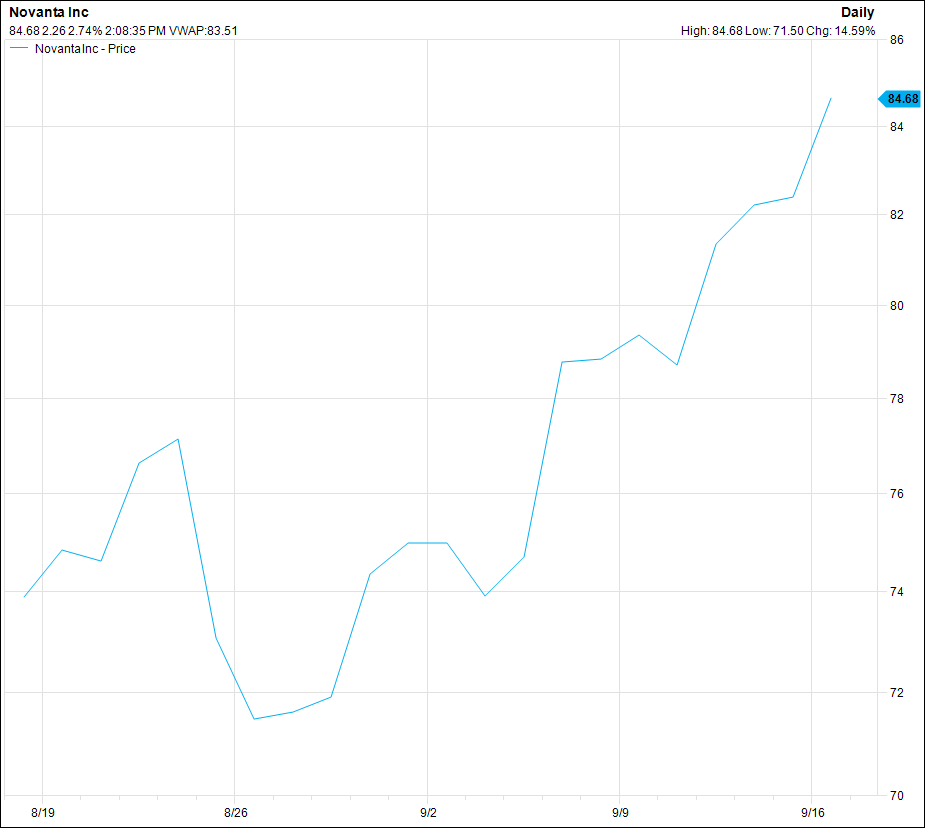

What

has the stock done lately?

After reporting earnings

on August 6th, the stock fell nearly 10% over the next several days

in response to disappointing commentary from management. Macroeconomic

headwinds remain a significant concern moving forward, and the market has

reflected that in the stock price. Novanta rebounded from a disappointing

August with a stellar September, driving the share price up more than 13%. The

stock has more than outperformed the broader market rally, as the Russell 2000

Growth index is up only 5.4% MTD. The company is not set to report earnings

until November 11th, so I don’t expect any significant price swings

until then.

Past

Year Performance:

Source:

FactSet

My

Takeaway:

I believe it may be time

for us to realize our gain on Novanta. The fund has realized a 53% gain from

Novanta since its addition to the portfolio, and is still trading relatively

near its July all-time high. The stock is simply too ‘growthy’ for me to stomach

in the current late-cycle climate. Management has relied on acquisitions to

inorganically grow revenues in the midst of macroeconomic uncertainty, and I am

not confident this strategy can continue to work in the future. High growth has

already been priced into the stock, and a sizeable drop in price could occur if

sizeable market expectations are not met. Additionally, management has been

artificially boosting earnings through questionable accounting. The subtraction

of ‘unusual expenses’, mainly arising from a continued history of M&A

activity, have provided EPS increases in each of the past 18 years! Despite the

artificial increases in earnings, the stock is trading at a 52.6 P/E multiple

and a 27.0 EV/EBITDA multiple, significantly higher than historical and peer

averages. For these reasons, I think it’s time to move this stock out of the

portfolio and add a value stock that is more suited for the late-cycle economic

environment.

Source:

FactSet