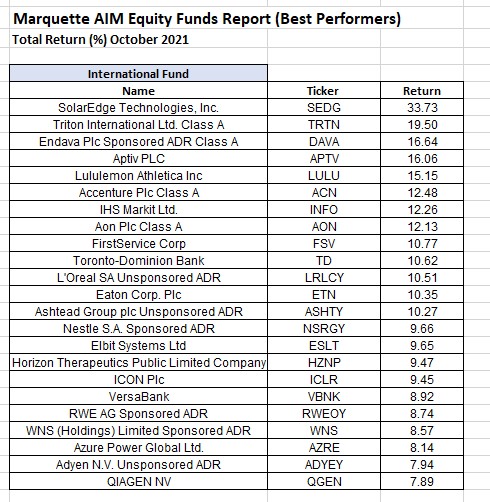

October produced some big returns in the AIM Small Cap and International Equity Funds

The Marquette AIM student-managed funds had a strong month of October. Check out the top performers in the Small Cap and International Equity Funds.

October produced some big returns in the AIM Small Cap and International Equity Funds

The Marquette AIM student-managed funds had a strong month of October. Check out the top performers in the Small Cap and International Equity Funds.

The fundamental equity analysis employed by the students in the Marquette AIM program works!

The Marquette AIM Student-Managed Equity Funds continue to produce impressive return performance. As of 10/31/21, both funds exceeded their benchmarks for the month, YTD, and 3-years. Although not reported here, the funds also have outperformed their benchmarks on a 5-year, 10-year, and 15-year basis. These resulted are even stronger on a risk-adjusted basis.

|

|

|||

|

Total Return

(%) |

|

|

|

|

|

|

|

|

|

|

Small Cap Fund |

Russell 2000 |

Excess Return |

|

October 2021 |

7.31 |

4.25 |

3.06 |

|

YTD 2021 |

20.12 |

17.78 |

2.34 |

|

3 Years |

75.33 |

62.93 |

12.40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

International Fund |

MSCI ACWI |

Excess Return |

|

October 2021 |

5.48 |

2.45 |

3.03 |

|

YTD 2021 |

17.76 |

8.80 |

8.96 |

|

3 Years |

61.72 |

44.89 |

16.83 |

BlackLine, Inc (BL, $126.23): "BlackLine’s Bottom-Line Surprise"

By: Graham

Pedersen, AIM Student at Marquette University

Disclosure:

The AIM Equity Fund currently holds this position. This article was written by

myself, and it expresses my own opinions. I am not receiving compensation for

it and I have no business relationship with any company whose stock is

mentioned in this article.

Summary

Key

points: BL reported Q2 2021 earnings of $0.15 per share, beating the consensus

estimate of $0.08 per share, representing an earnings surprise of 87.5%. BL posted

$102.12 million in revenues for the quarter ending June 2021, surpassing the consensus

estimate of $101.1 million. BL showed revenue growth of 22.6% year-over-year,

and its price-to-earnings ratio is currently 193.5. The company has

outperformed consensus EPS forecasts four times over the last four quarters.

The BlackLine Optimization

Academy consists of training sessions that focus on nine foundational

accounting processes to improve efficiency in automation with BL. In addition,

the initiative seeks to help customers get the most value out of BlackLine by

proactively engaging them earlier in the transformation process. As a result, BL

can expect to experience increased adoption and platform expansion as clients

realize the full benefits of the service.

While the effects of the pandemic

are subsiding, BL has seen an increasing trend in large companies prioritizing

digital transformation. As a result, executives are being asked to perform more

with the same or even fewer resources in today's organizations, which are

experiencing a severe skills crisis. BL can capitalize on this by automating

time-consuming and laborious activities, thus freeing critical finance and

accounting resources.

BlackLine’s SolEx deals were vast

and strategic in scope, covering APAC, EMEA, and North America. SolEx was

especially strong in the APAC region, creating significant orders and

building its small growing business in Japan. BL expects to continue

capturing new SolEx accounts through partnerships.

What has the stock done lately?

BL’s share price has consolidated

within the $110s/$120s over the past month and hasn’t shown any signs of a break-out.

From year to date, BL shares have fallen 7.5%, compared to a gain of 20.8% for

the S&P 500. The stock's 50-day moving average is $116, and its 200-day

moving average is $117. The Q1 2021 consensus EPS forecast is $0.13 on revenues

of $107.5 million and $0.48 for the current fiscal year on revenues of $420

million.

Past

Year Performance:

Shares of BlackLine, Inc. have

been trading within a range of $154.61 and $88.62 over the last 52-week period.

BL has experienced a YTD loss of -7.52%, with a 52-week beta of 1.25. BL was

closely shadowing the Russell 2000 (Figure 1), although BL fell sharply in

March and continued to lag while the Russell 2000 continued sideways. BL has underperformed

the benchmark from year-to-date, producing a 52-week gain of 22.13%, compared

to the benchmark at 39.52%.

My

Takeaway

BL was added to the small-cap

portfolio in March 2017 at around $27.50 per share, with a price target of

$32.99. Since being added to the fund, the stock has gained over 348%. BL was

pitched under the notion that expanding through international- and

middle-market penetration would drive top and bottom-line growth. Management

has demonstrated strong performance, quadrupling the firm’s size over four

years, reducing the WACC by 44%, and generating positive ROIC, ROA, and ROE

since added. Because the investment thesis continues to support long-term

growth and profitability, I believe that BL represents a hold in the AIM

small-cap equity fund.

AIM Class of 2022 Student Equity Presentations on Friday, October 29th

Join us live in person in the AIM Room or via Teams for this week’s AIM presentations beginning at 1:00 pm.

This is the link for the AIM equity write-ups

(each week’s write-ups will be available on Thursday mornings): AIM Write-ups 10/29/21

This is the link for the YouTube videos of the 8-minute student presentations (each week these will be posted on Thursday afternoons)

If you would like to participate in the live Q&A session with

the student presenters on Friday at 1:00 pm CST on Teams, please email

Jessica Hoerres at: jessica.hoerres@marquette.edu

Please feel free to submit questions to be asked of the students by emailing them to david.krause@marquette.edu

Beam Global (BEEM 28.75): “Running Low on Battery”

By: Jacob

Kello, AIM Student at Marquette University

Summary

KEY POINTS

In the year 2020, the

global electric vehicle (EV) market size was valued at $246.74 Billion, which

was down 9.7% from 2019 due to the global COVID-19 pandemic. However, Fortune

Business Insights, a company which specializes in the research of sectors,

projects that by 2027, the EV market will grow to 985.72 billion USD which

represents a CAGR of 17.4%. In unit terms, the global EV market demand was

estimated at 8.5 million vehicles in 2020 and is projected to reach 116 million

units by 2030 according to Bloomberg New Energy Finance. Demand for EV’s

clearly exists and is being met by newer EV companies and some traditionally

internal-combustion engine auto companies which are now producing more EV

lines. While the demand for Electric vehicles clearly exists, the demand for

public charging stations has stalled due to slow-moving infrastructure bills,

and the Biden Administration’s climate agenda no longer being a part of the

bill. This unfortunately has some not-so-great implications for a stock in the

AIM Small Cap Domestic Fund—Beam Global.

The most important driver of

earnings for BEEM was its GSA MAS contract with the federal government that

allows federal institutions to purchase EV Charging products specifically from

BEEM Global. At the beginning of the new presidency, the Biden administration

also had committed to deploying over 500,000 EV charging stations by 2030. This

commitment was clearly contingent on a climate-centric infrastructure bill, and

it was very recently announced that the administration’s climate agenda will be

completely removed from the bill due to opposition within the democratic party

coming mainly from West Virginia Democratic Senator Joe Manchin.

The company has yet to turn a

profit, and it doesn’t look like it will by 2025 which is when it was projected

to turn a profit when it was bought by the fund. Even with the levelized cost

of energy for photovoltaic solar being the lowest it has ever been and

continuing to decrease, materials costs to produce solar panels and batteries

have continually increased which obviously hurts a company that relies on solar

power storage to charge electric vehicles.

What has the stock done lately?

Recently, the stock has been

fairly stagnant. Since May of 2021, the stock has continuously above and below

$30, and since adding the stock to the Small Cap Domestic Fund, it has gone

down by 40.65%. On October 7th, the company released news that they

had received an order from the United States Marine Corps to purchase EV Arc

and energy resiliency systems for 14 of their bases, and the per share price

only rose 2.4% by the end of the week. This stock is stagnant, and will

continue to be stagnant unless the infrastructure bill includes climate

provisions which is looking unlikely.

Past Year Performance

BEEM has fallen 61.03% YTD and over a

52-week period has increased by 85.01%. The 52-week high-low for AMRC is 14.15

– 75.90. The 52 week beta for Beam Global is 2.8, representing very high

volatility in comparison to the market.

My Takeaway

The investment thesis for BEEM global

has yet to pan out and does not look like it will anytime soon. The upside for

BEEM was heavily dependent on their GSA MAS contract with the federal

government, and that contract was also dependent on the infrastructure bill

that congress was expected to have passed long ago. Also, with Senator Joe

Manchin stalling any action in regards to a climate bill, it is not expected

that the most important driver for this stock will pan out anytime soon. With

that being said, it is recommended that BEEM should be sold and taken out of

the AIM Small Cap Domestic Fund.

Insight Enterprises, Inc. (NSIT, $93.56): “Continued Growth Insight”

By: Will

Steinhafel, AIM Student at Marquette University

Summary

Key

points: On August 6, 2021, Insight Enterprises reported Q2 EPS of

$1.91/share, beating consensus estimates of $1.87. Revenue also surpassed

expectations at $2.23 billion, representing a 13.26% YoY increase. This

impressive quarter was driven by strong hardware demand, as well as SaaS and

Infrastructure-as-a-Service (IaaS) sales growing at high double digits during

the quarter.

Despite ongoing supply

constraints due to Covid-19 disruptions, management is confinement in Insight’s

ability to continue to work with customers to forecast demand moving forward.

In NSIT’s Q2 earnings call, management shared that they project over 50% of the

company’s backlog will be shipped during Q3 FY21. NSIT’s supply chain and

product pipeline is expected to normalize and return to healthy growth during

the second half of FY 2022.

Insight is aiming to grow its

cloud solutions business through the development and sales of SaaS and

Infrastructure-as-a-service offerings. As previously mentioned, NSIT saw strong

growth of these product lines during Q2, resulting in cloud gross profit

increasing over 300 bps YoY to 22%. Management is dedicated to growing Insight’s

cloud offerings moving forward to continue revenue growth and margin

improvement.

What

has the stock done lately?

Insight’s share price has

remained relatively flat over the last month, with a -0.65% decrease during the

period. NSIT beat Q2 FY21 consensus earnings by $0.04, reporting EPS of $1.91

representing a 9.14% YoY increase.

Past

Year Performance:

Over the last year, NSIT’s share

price has increased 47%. The 52-week high-low for NSIT has ranged from $107.27

to $52.63. As of Q2 FY21, Insight posted all time high LTM revenues of $8.65

billion. Since being added to the AIM Small Cap fund in September 2020, NSIT’s

share price has increased 56%.

My

Takeaway

Since being added to the AIM

Small Cap fund in September 2020, Insight Enterprises has well surpassed its

price target of $87.86, however, the initial investment thesis remains intact.

NSIT is poised to continue to benefit from increased demand as businesses look

to shift to cloud-based solutions and modern technology infrastructure. As

management focuses on SaaS and IaaS offerings, continued margin expansion can

be expected due to decreased cost of goods sold. It is recommended that the AIM

Small Cap fund continue to hold Insight Enterprises.

TechTarget, Inc. (TTGT, $82.74): “On Target to Exceed Expectations”

By: Natalie

Frey, AIM Student at Marquette University

Summary

Key

points: TechTarget, Inc. remains 'in-play'. While the price saw little

movement during Q2 and most of Q3, toward the later months of the third quarter

the stock began to gain traction. Currently, TTGT stands at $82.74 per share,

which is up approximately 8% from its addition to the fund. While this growth

in share price demonstrates positive movement, the stock has not yet lived out

the thesis which states a target price of $92.70.

Given the positive earnings surprises

seen in Q2, the original thesis appears to hold true at this time in its

argument that TTGT still has room to grow. During 2020, TechTarget acquired

BrightTALK, a webinar hosting platform primarily to expand the firm’s reach

into the corporate IT market. During 2021, BrightTALK registered users have

been integrated into the Priority Engine product offered by TTGT and this has

provided revenue synergies above previous expectations for Q2 of 2021. With

synergies resulting from the acquisition hitting TTGT’s P&L faster and at a

greater level than originally expected, the markets are favorably surprised by

the firm’s agility in creating value from strategic acquisitions. This provides

good reason to be optimistic about the likely benefits to come from the recent acquisition

of Xtelligent.

In addition to the favorable

impacts of prior year acquisitions, TechTarget announced a new product during

the summer of 2021. The product that was announced in June was the new and

improved version of the legacy product, Priority Engine. The new version adds

significant enhancements to the legacy platform with account visibility that is

2x that of the legacy system and enhanced access to content consumption information.

While these additions may seem like minor refinements of existing features, the

impact for sales reps utilizing TTGT has been significant.

With the successful integration

of BrightTALK users into TechTarget’s core platform, the impactful new product launch,

and continued focus on growth and improvement of existing product lines, TTGT

is on a steady path to achieving a higher value. The consensus analyst recommendation

supports this argument, with the average price target having risen to ~$100.

What

has the stock done lately?

Since the release of Q2 earnings,

the stock has risen approximately 12%. The positive earnings surprise has the

market taking a second look at their expectations for TechTarget’s growth

potential. The recent momentum demonstrates the likely start of a gradual climb

for TTGT’s share price in the coming months.

Past

Year Performance: The YTD returns stand at 37.5% for TTGT, with the

1Y return rising to 64.4%. The YTD returns demonstrate impressive growth, but TechTarget

remains undervalued according to the original thesis the stock was pitched on and

much of the street’s valuation estimates. With the price beginning to climb after

a multi-month stretch of low movement, TTGT’s share price is likely to continue

climbing in the near-term.

My

Takeaway

TechTarget’s success in integrating

BrightTALK’s registered users into the core product platform has driven synergies

that exceed expectations, both in magnitude and time of realization. The release

of a positively received new version of Priority Engine has expanded the value

offered by TechTarget’s products and services for both clients, and end-buyers.

With high quality content, the buyers of corporate IT are able to access

high-quality information and be efficiently connected to sellers based on

consumption data. The sellers of IT have even more to gain from TTGT’s enhanced

offerings and increased user base, making top choice in sales development

tools.

Vestas

Wind Systems ADR(VWDRY, $82.39): “Is there still wind at

its back?”

By: Bob Thelen,

AIM Student at Marquette University

Summary

Key

points:

Vestas

Wind Systems remains a stable company as they continue to expand production of various

wind turbine systems. The firm has consistently grown sales figures from $9.3

billion in 2015 to $16.8 billion in 2020 although net income has been stagnant from

a 2015 figure of $760 million to a 2020 figure of $872 million.

Vestas maintained

a current ratio of at least 1.1 since 2014 as they utilize the majority of

their assets for leverage in expanding production and development of new systems.

The firm also has a Debt/Equity ratio of 29.1% which puts them at very low risk

of encountering debt issues in the near future. While Vestas has encountered

slow growth in the past, their capital structure shows that they are prepared

to take advantage of the increasing international demand for wind power systems.

As Vestas continues to accept new

contracts for various international clientele, they stand to benefit from global

trends towards wind and solar power generation and are steadily increasing capital

expenditures to a high of $901 million in 2021 (LTM), up significantly from

$408 million in 2015.

What has the stock done lately?

Vestas

has been up since March of 2020 with a current share price of $11.55 and has

been in a range of $11 to $15 for the majority of 2021 as no major news has

affected its share price since January of 2021 when it received regulatory

approval on a joint venture with Mitsubishi Heavy Industries.

Past

Year Performance: Vestas share price has not increased in value over

the past year as a result of a sharp increase in January of 2021 due to approval

for a joint venture with Mitsubishi Industries, but fell due to a market

correction.: Vestas’ valuation implies a steep discount with a broker price

target of $75.25. While unlikely to hit this target in the near term, it has

the potential to achieve this by taking advantage of the rapidly expanding wind

power segment.

Vestas is

proving to be a major player in the development and production of the wind

power industry and will stand to benefit from global trends toward renewable energy

sources. While they have experienced slow growth and a stagnant share price over

the past few years, they are ramping up to provide an increasing customer base

with wind power solutions. If Vestas can take advantage of this growing market,

then they will be able to achieve the lofty price target set by various

brokers.

SoFi Technologies (SOFI, $18.39): “SoFlying into the future of banking”

By: Rishi

Kumar, AIM Student at Marquette University

Disclosure:

The AIM Equity Fund currently holds this position. This article was written by

myself, and it expresses my own opinions. I am not receiving compensation for

it and I have no business relationship with any company whose stock is

mentioned in this article.

Summary

Key

points: SoFi had a disappointing earning in

August which caused share prices to plummet to $13.75. However interestingly enough

SoFi’s CEO Anthony Noto was thoroughly impressed with the performance of the company

as they recorded their fourth straight quarter of positive adjusted EBITDA and

grew every key performance measure.

Revenues

for SoFi grew 101% to $231M in Q2 beating street estimates by 6% while total

members rose 117% to 2.6 million. The financial services segment grew 608% to

$17M while the financial technologies segment represented by the Galileo platform

acquired last year grew accounts 119% to 78.9 million accounts while growing

revenues 138% to $45.3 million.

However,

despite the growth EPS came to -0.48 vs the expected -0.06 EPS causing the

street as well as investors to become weary. However, the EPS was slightly misleading

as much of it can be tied to non cash one time non-cash items. Most prominently

was a one-time non-cash cost related to deferred tax liabilities of 99.8M which

were tied the Galileo acquisition and 89M could be tied to stock based

compensation. Also, the company’s positive adjusted EBITDA and user metrics were

not considered by the street which are more relevant for an aggressively

growing financial technology company rather than an EPS figure.

Since then,

SoFi’s shares have rebounded quite nicely, going up nearly 25% since the

earnings call. Much of that outperformance can actually be tied to a sell side

initiation report published by Morgan Stanley on October 11th, 2021,

which caused share prices to climb 13.45%. According to Betsy Graseck, the

analyst at Morgan Stanley who initiated coverage, SoFi is a disruptive company that

has a “powerful growth story” and according to Graseck SoFi has two major

growth catalysts: student loan refinancing and the bank charter SoFi is actively

pursuing.

Student

loan refinancing was SoFi’s first initial claim to fame as they became famous

for having some of the lowest student loan refinancing rates among legacy

players and challengers. The student loan space is ripe for this kind of mass

refinancing, according to a study done by Andrew Latham at Supermoney[1], student loans have been the fastest growing debt

in US households since 2007 with 32x faster growth than mortgages and 3x faster

growth than auto loans. This would give SoFi a huge tailwind as student loan

deferments end at the end of January 2022 especially with a large base of potential

customers in the United States who have student loans.

SoFi

will also benefit from a second major driver according to Morgan Stanley which

is the procurement of a bank charter. A bank charter allows SoFi to underwrite

their own loans instead of using bank partners which in turn leads to margin

expansion and increased profitability. According to SoFi’s last investor presentation

a bank charter would result in adjusted EBITDA rising from $254M to $447M and

growing at a CAGR of 143% as opposed to 130% from 2021 to 2025. The lower cost

of capital and the ability to capitalize on their own deposits while also cross

selling loan products to other digital banks via the Galileo platform will

drive incremental growth in revenue and margins.

In

recent news, SoFi announced a proposal to issue $1.1 billion in unsecured convertible

notes that are due in 2026 with an interest rate of 0% and a conversion price

of $22.41. The increased liquidity will be used to build out SoFi’s platform

without the company having to incur heavy interest expenses. The initial notes

proposed were for $750M but management appended the figure to $1.1 billion to

capitalize on the low cost of debt.

What

has the stock done lately?

The

stock has had quite the pop recently as mentioned earlier due to the sell side

report and due to the gross misunderstanding of earnings by the street and

investors who grew wary by the higher than expected negative EPS. The stock

went up 13.45% on October 11th and since their last earning call

shares have risen considerably. . The next earnings call is set to take place on

November 10th, 2021.

Past Year Performance: SoFi’s SPAC merger was less than a year ago so share prices are up ~84% since the merger was announced however the stock is still down from its 52-Week high of $25.78. Overall negative sentiment towards SPAC’s and less than stellar EPS in recent quarters has brought down share prices.

My

Takeaway

With strong user and revenue growth

metrics and a business model that is sticky due to the one stop shop nature of

the business, SoFi is still in optimal position to keep growing revenues

aggressively and expand margins through the procurement of a bank charter. The

street is starting to account for the strong growth in users and consistent

positive EBITDA as evidenced by Morgan Stanley’s initiation report. SoFi’s

lower rates, rounded product lineup, and completely digitized platform gives

them a significant advantage over their big bank peers and the thesis on which SoFi

was pitched remains strong as the technology segment is still seeing 100+% growth

and consumers are flocking to SoFi’s robust platform. Due to these reasons I

believe SoFi’s stock is still undervalued and it is recommended that the AIM

small cap fund continue to hold SoFi shares in the portfolio.