Marquette Applied Investment Management (AIM) Program

End-of-the-Year Newsletter (Winter 2020)

The following link contains the most recent AIM Newsletter:

Marquette Applied Investment Management (AIM) Program

End-of-the-Year Newsletter (Winter 2020)

The following link contains the most recent AIM Newsletter:

Medtronic Plc (MDT, $113.70): “Where to next for Medtronic?”

By: Ryan Witt, AIM Student at Marquette University

Summary

• Medtronic Plc (NYSE:MDT) is a medical technology company that provides medical devices, solutions, and services. The segments MDT operates through are their Cardiac and Vascular Group (36.2%), Minimally Invasive Technologies Group (28.9%), Restorative Therapies Group (26.7%), and Diabetes Group (8.7%).

• Since MDT was added to the AIM International Equity fund in October of 2017 for $78.24, MDT has increased 45.3% and exceeded its initial price target of $92.27.

• MDT saw 53% of its FY21 Q2 revenues come from the US, while the company also operates in more than 150 countries.

• For FY21 Q2, MDT experienced a -1.5% decrease in revenue from FY20 Q2 due to the impact of COVID, but did rebound to increase 17.5% from FY21 Q1.

• Geoffrey S. Martha was named CEO as of April 27, 2020 following the 9 year run of Omar Ishrak as CEO, who now is the current Executive Chairman of the Board.

Key points:

MDT has started the restructuring to change their organizational structure with a new simplified model which is expected to save them $450 -$475 million by FY23. Martha has said he wants to turn the current operating groups and transition them into very focused operating units. Doing so will allow MDT to give each operating unit more control over their specific segment and allow them to be accountable for their own specified unit.

Martha is hoping to form 20 operating units from the larger overall company. These operating units would be separated under the four different segments. By doing this Martha believes that MDT will be able to obtain organic sales growth of 5%-plus for the long-term by reorganizing the company. There is some skepticism with this as the company has not been able to hit 5%-plus in the past few years.

With MDT being the largest player in the medical technology market and having a constantly expanding product line with numerous products from its pipeline, it has been seen that since the start of 2020 MDT has had over 180 product approvals in key geographic regions. This will continue to grow as MDT expands into new business segments and through their acquisitions. MDT has completed seven acquisitions in 2020 for a combined $1.6 billion furthering their expansion into AI, machine learning, and predicative analytics.

MDT has increased its dividend for every fiscal year going back 43 years. They are on similar path to do so this year coming out to annual dividend per share of $2.32 for FY21. An increase of 7.4% from the FY20 which was $2.16 per share. MDT has no plans of scaling back on dividends and plans to increase them in the future as well.

What has the stock done lately?

MDT took an initial hit from the coronavirus pandemic, but has seen some bounce with a 3 month change of 5.41%. For November the stock has increased 12.6% on the back of the recent vaccine news that saw the market jump. MDT has paid two dividends of $0.58 per share out to shareholders for FY21 Q1 and Q2. The company still plans on paying the same for Q3 and Q4 despite the pandemic.

Past Year Performance: Over the past 12 months, MDT has seen a change of 2.07% over the year compared to the ACWX-USA(iShares MSCI ACWI ex U.S. ETF) which is up 6.39% for the year. Over the past year MDT has seen a decrease in sales of -5.4%, but increase of net income of 3.4%. Throughout the year MDT has had a range of $72.13 – 122.15. The current price of MDT is $113.70.

Source: FactSet

My Takeaway

Being one of the biggest players in the Medical technology for years now, MDT certainly has an advantage over the competition with its size and plethora of products. However, the pandemic did recently effect MDT in the final quarters of FY20 and beginning quarters of FY21. Although I believe that the company is promising for more growth in the future, the uncertainty around the new CEO and his massive restructuring plan for the coming years have me wary of increasing the weight of MDT within the AIM International Equity Fund. For this reason my recommendation would be a hold as I still think there are opportunities for growth down the line, but the skepticism of the bold restructuring of the organization is prevalent.

Source: FactSet

Hamilton Lane, Inc. (HLNE, $75.26): “Continuing Down the Lane for Profits”

By: Ben L’Empereur, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with any company whose stock is mentioned in this article.

Summary

• Hamilton Lane, Inc. (NASDAQ: HLNE) is one of the largest global private market investment managers. They work with their clients to buy, manage, and sell funds and investments. Their clients include investors from the United States, Europe, the Middle East, Asia, Australia, and Latin America.

• EPS is up from $0.02 in Q1 of FY2021 in June to $0.66 to Q2 as reported on November 4th. This increase nearly brings EPS back to HLNE’s pre-COVID number of $0.74

• From Q2 of FY2020 to Q2 of FY 2021, total assets under management grew nearly 11% from year-to-year to $73 billion. Fee-earning assets grew by almost 9% to reach $39 billion in the same period.

• HLNE builds and customizes private market funds to meet each of their customer needs. This segment of revenue accounts for $57 billion of their AUM. Their advisory service segment holds nearly $474 billion assets under advisory for some of the largest private market investors in the world.

• HLNE continues to expand worldwide. The company announced on October 28th, 2020 that they just opened an office in Singapore. This office is the 5th location they now have in the Asia Pacific area.

Key points: Hamilton Lane, Inc has yet to reach its peak when considering their growth potential. With the FOMC projecting interest rates to stay near 0% for the next couple of years, there is a higher demand for investment services. Consumers would rather put their excess income in riskier assets with a higher chance of return than settle for next-to-nothing gains on their investments.

With more investors moving towards the use of FinTech, HLNE already has significant technological developments that sets them apart from their peers. Bundled into their investment solutions offerings is a wide variety of data analytics monitoring their client’s investments and reporting real-time data. For an industry that is important to monitor and report timely information on, Hamilton Lane has already differentiated themselves from the competition.

The company also has a strong management team who have years of experience with the company and within the industry. As the firm continues to navigate the difficulties COVID-19 poses and a transition to a more technology-based investment environment, it is reassuring to be led by a management company that knows the company inside and out.

HLNE provides investment services to institutional investors all over the world. Their revenue has grown double digits year-to-year in countries like Mainland China, Japan, France, and Italy. With their continuous global expansion and effort to open offices in different countries, HLNE will continue to grow their market share in the United States and internationally.

What has the stock done lately?

Following a nearly 20% drop in stock price due to the announcement of a new stock issuance, HLNE has been steadily increasing for the past 3 months. As of November 16th, it had hit a 52-week high at $76.42. As the market continues to recover from the COVID-19 pandemic, and the confidence in a vaccine become stronger, the price will continue to increase.

Past Year Performance: HLNE has increased 32.70% in value over the past year, even with the effect of the selloff in March after news of the nation-wide lockdown was announced. In the past year, HLNE has outperformed the benchmark 22.79%. Since it has been purchased at the end of September, the stock has posted about an 18% gain.

Source: FactSet

My Takeaway

Hamilton Lane, Inc. still has a very bright future ahead of them with a lot of growth potential. As reflected in the consistent rise in the price of the stock for the past three months, investors are confident in this firm’s ability to grow its bottom line and market share. With the hopes of a vaccine and an economic recovery, the firm has more potential as investors have more excess income. I recommend that we hold the stock for the foreseeable future to benefit from HLNE’s future growth.

Source: FactSet

Nexstar Media Group Inc. (NXST, $109.35): “And our Nexstar in the industry is…”

By: Holden Patterson, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with any company whose stock is mentioned in this article.

Summary

• Nexstar Media Group Inc. (NASDAQ: NXST) is a television broadcasting and digital media company that operates all across the United States. In addition to operating local television stations, they also develop many local interactive community websites and provide digital media services.

• NXST will be brining NEXTGEN TV, a new IP broadcasting system that lets internet content be transmitted through over-the-air broadcast signals, to their local station in Raleigh, NC.

• NXST recorded record net revenue of $1,118.2 million in Q3 of 2020 which was 68.5% higher than Q3 of 2019.

• NXST capitalized on the United States electins in 2020, bringing in 132.4 million of political revenue during Q3.

• In September, NXST launched WGN America’s primetime national newscast, News Nation, in addition to the mobile app, NewsNationNow, helping them reach millions of users.

• NXST repurchased1,300,000 shares of its Class A common stock at an average price of around $96.14 per share.

Key points: Nexstar is one of the major broadcasters that will be brining NEXTGEN Tv to their local television station in Raleigh, NC. NEXTGEN TV is an Internet Protocol (IP) based system that can transmit internet content and services over the traditional over-the-air broadcast signal. This technology will improve signal, give greater sound and higher quality picture, expand transmitting distance, and provide additional features such as video-on-demand.

NXST recorded record net revenue of $1,118.2 million in Q3 of 2020. This was 68.5% higher than Q3 of 2019. Of the third quarter television advertising revenue of $514.3 million, 132.4 million is political revenue and $381.9 million is core advertising revenue. Although it is unlikely that they will maintain this high level of political revenue after the presidential election coverage comes to an end, they were able to capitalize on this huge event.

NXST launched WGN America’s primetime national newscast on September 1st, News Nation, which is viewed by around 75 million television households across the country. This launch also came with an accompanying mobile app, NewsNationNow which gives their audience the ability to follow their stories and coverage with the simplicity of their smartphone.

NXST recently repurchased a total of 1,300,000 shares of its Class A common stock at an average price of $96.14 per share for a total cost of $125 million. This was funded from cash flow from operations. NXST CEO, Perry Sook, says quarterly cash dividends and share repurchases will continue to be a priority of their capital allocation.

What has the stock done lately? After taking a huge hit at the start of the pandemic in March, NXST has started to move back towards where it was at in the beginning of 2020. YTD the stock has decreased by 5.19%, but since they hit a low of $43.37 at the end of march the stock has increased by 152.13% to $109.35 today.

Past Year Performance: NXST has not yet retuned to the level they were trading at in January and February of 2020 but has recovered nicely from the pandemic. Sitting around $109.35, NXST has seen a steady growth of around 2% for the past 52 weeks. This is promising to consider the massive hit they suffered at the start of the pandemic. They have followed a very similar pattern as the Russel 2000 index but have consistently seen lower levels of return over this past year.

Source: FactSet

My Takeaway

NXST is right where they need to be. They have done a great job reacting to the pandemic which is seen by their record net revenue growth in Q3 and are effectively moving in the direction their industry is going. I believe this is a stock that we will see do quite well in the next couple years as they continue to rollout technology such as NEXTGEN TV into more and more cities to combat against the internet of things movement. This stock should be held in the AIM portfolio until their business becomes unable to keep up with where the television/media industry is moving.

Source: FactSet

Uniti Group Inc. (UNIT, $10.16) “Covid Resistant and Growing”

By: Elisabeth Desmarais, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with any company whose stock is mentioned in this article.

Summary

• Uniti Group Inc. (NASDAQ: UNIT) is a unique real estate investment trust (REIT) that focuses on acquiring and building infrastructures in the communication industry. The fiber network focused company operated in the following segments: Leasing, Fiber Infrastructure, Towers, Consumer CLEC, and corporate.

• While the COVID pandemic is hurting many industries badly, the telecom one is not part of them.

• The first driver of UNITI’s pitch from this past September was the current upcoming high demand or Fiber Optic Network during the pandemic. The trends and obligations to stay at home and quarantine increased this demand and need for most people.

• Another driver included Windstream’s Bankruptcy Emergence. At first, the bankruptcy created some uncertainty from the investors in how UNITI will be able to pay their dividend and bounce back since the stock was strongly impacted by this event. However, this gives the company a lot of room to increase the business operations as well as their paid dividends.

• Windstream who takes a huge part of the organization’s business finally file out of Chapter 11 bankruptcy on September 21st. The company has a good amount on hand at the moment to fuel growth but was also able to get rid of $4 billion in debt, thus a great positive for both companies.

Key points: Uniti Group is strongly dependent on Windstream which account for approximately 65% of the company’s revenue. According to that, the coming out of bankruptcy for Windstream was a positive hit for UNITI. Windstream’s CEO, Tony Thomas, mentioned the importance of reaching this milestone, thus leading to a healthier financial and liquidity standpoint for the company.

While Windstream was part of the big risk of the company, it has to keep a high market share, however, we can be assured that the fiber industry is not too competitive, and that Windstream should be able to cover the 30% of market share they are aiming for.

Moreover, in the latest third quarter report, the company announced a strategic transaction with Everstream Solutions LLC. This new OpCo-ProCo deal with Everstram includes two 20-year IRU lease agreements which will be covered in 8 states, thus 10,000 route miles and 220,000 stand miles. The cash consideration for Uniti after selling some of their Northeast operations to Everstream plus the IRU payments will equal an approximate of $135 million.

In addition, the company was officially pitch due to its very unique business model and offerings. The company still has a lot of drivers and opportunities in front of them. The presence and growth of 5G plays a role in the business and the need for greater bandwidth and faster speed connections will remain as a driver of UNIT. However, the consideration of high cost of installation during this economic period can be uncertain.

While on the drivers of in the pitch of this stock was the dividend policy certainty, it not exactly the case, considering that might actually be uncertain even with the consideration of Windstream bankruptcy emergence. UNIT who was projected to have the covenants lifted once it reaches a 5.75x net leverage, which will likely not happen in the next two following years. The company is a fast growing one, however, not in the dividend aspect like it was projected to be.

What has the stock done lately?

The company has continued its growing strategy by acquiring new fiber networks operators. These acquisitions include Southern Light and PEG Bandwidth. In October, Uniti Group has purchased Information Transport Solution (ITS), a company who provides connectivity services while having a main focus on educational clients. The company has also declared a cash dividend of $0.15 per common share for the quarter.

Past Year Performance: From November 5th announcements, the company has leverage ratio at quarter of 6.1 times, based on the net debt annualized adjusted EBITDA. In addition of AFFO per share of $0.42 for the third quarter and $258.8 million revenue. With a current price of 10.16, the stock price has been going up, slowly, for the past year. UNIT’s revenue from Windstream has decrease to 64% from 70% about a year ago.

Source: FactSet

My Takeaway

The company previous legacy, Windstream, fill out for bankruptcy earlier on and got out of it this year on September 21st, thus bringing prosperity to UNITI and its new settlement with the company. The settlement of litigation of Windstream who constitute a great part of the business revenue has been successful. The company has also expanded its operations with the acquirement of new entities with different stands such ad OpCo-ProCo transaction resulting in independent financial and credit terms. UNIT’s diversification strategy and goal of decreasing its revenue percentage from Windstream has come to life, however, it is still not close to its final goal of having 50% of their revenue from them.

Source: FactSet

Dicks Sporting Goods (DKS, $58.51): “Sports are back Stronger than Ever”

By: Matt Schembari, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with any company whose stock is mentioned in this article.

Summary:

• Dick’s Sporting Goods, Inc. (NYSE: DKS) is a full-line sport store that is located in the United States. They have carried apparels from all the big sporting companies.

• Dick’s Sporting Goods has extreme loyal costumer, with their Scorecard Loyalty Program brining in 70% of their sales. This is important with all the uncertainties in the world with COVID-19.

• Dick’s Sporting Goods has had a big e-commerce year due to COIVD. They are also in many long-term real estate investments which can limit Dick’s ability to switch out of some locations.

• Dick’s Sporting Goods has stayed in the family. The current CEO is Edward Stack, and he is the son of Dick Stack who founded the company.

• Although in quarter two for Dick’s was the main reason why their growth YOY was 42%. I believe there will be an increase in quarter four.

Key points: Dicks Sporting Goods remains a very promising Stock with the ability to continue and have a great fourth quarter. During the third quarter their revenue ended at 2.24 billion. They have also increased EPS by 1.05 during the third quarter, and I only see it growing headed into the fourth quarter. They also hold a higher gross margin then most of their competitors during the quarter three.

Dick’s Sporting Goods has been adapting well to COVID. Every company has had to make changes constantly and are trying to figure out the best ways to still make a profit while making their employees happy. Dick’s did end up having to close 15% of the stores which they own. This would cause some worry to some companies, but Dick’s focused their attention on making their e-commerce stronger. Dick’s was able to increase their e-commerce sales by 160%. Secondly, with the COVID they have focused on pushing more social distanced sporting products such as golf, which has increased almost 50% during COVID.

Dick’s Sporting Goods also has a great private label. They have been focusing on growing this more recently. Dick’s does a great job offering items that are well represented from the NCAA, NBA, and FIFA. This gives them a great source of revenue from well-known apparel distributors. They also have a great private brand which brings in 14% of their sales. This is only behind Nike which is one of the most well-respected sporting apparel stores in the world.

DKS is trying to constantly give back to the community and know everyone is struggling during this challenging time. Dick’s Sporting Good teamed up with LISC in early November to invest in more the $12 million to the Black Economic Development Fund. This fund is to help lower the racial wealth gap. Dick’s Sporting Goods also is offering a “10 Day of Black Friday”. The reason of this is to offer people sales for a longer period and to try to limit the crowded stores on Black Friday.

What has the stock done lately?

Since early November till currently there has been an increase in the stocks price. It has increased more the $5 EPS in the last month, which came at the same time of investing 12 million into the Black Economic Development Fund. Over the past quarter the price of the stock have gone up almost $4 per share. The increase over the entire quarter and the increase in the past month shows the company is on a strong trend upward.

Past Year Performance: DKS has increased the valuation by 20.79% over the past year. While saying this I do believe the company is still very strong and still currently being undervalued. The 52-week range has been $13.46 - $63.29. This is an extremely large range which seems so big but can be reasoned with the fact that COVID-19 happened. With the growing of e-commerce sales of 160% over the last year DKS has great upside.

Source: FactSet

My Takeaway

Dick’s Sporting Goods constant growth in the e-commerce section of the company is growing more than this last year with an increase of 160%. Even though there was a slight drop in sales in the third quarter I believe there will be a bigger increase in the fourth quarter. Dick’s has a great private brand that they are trying to grow, along with bringing in sporting apparels from key sporting vendors like the NBA, NCAA, and FIFA. Finally, DKS is constantly trying to offer and help the community around them by offering a longer black Friday sales in order to lower the spread of COVID-19 and also investing in the Black Economic Development Fund.

Source: FactSet

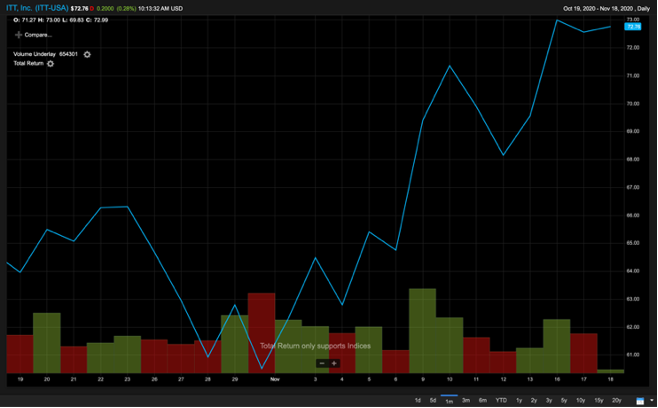

ITT, Inc. (ITT, $72.76): “A New Drive Forward”

By: Drew Kolz, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by

myself, and it expresses my own opinions. I am not receiving compensation for it and I have no

business relationship with any company whose stock is mentioned in this article

Summary

· ITT, Inc. (NYSE: ITT) engages in the engineering of products and solutions for the industries of energy, transportation, and industrial markets. ITT sells their products to companies in the United States and EMEA.

· ITT has approximately $1.5 billion in available liquidity. They are showing a great effort to expand their financial flexibility in hopes of making more investments in the near future.

· While the automotive industry overall suffered during the pandemic, ITT’s demand for their friction brake continues to rise.

· ITT is located in over 125 countries and has a set of very well diversified brand/product lines that has helped them weather the storm.

Key Points:

A main strength of ITT is their strong balance sheet. With $782.3 million in cash, $490.2 million in short-term receivables, and over $1.5 billion in total liquidity, ITT has given itself a great opportunity to increase their market share. Given that so many other competitors in the automotive and aerospace industries have not been able to withstand the effects of the pandemic, increased acquisitions and mergers should be seen in the near future by ITT.

Acquisitions made by the team in 2019 continue to produce great benefits for the company as a whole. The two acquisitions of RPG and Matrix Composites have led to direct increases in both production time and sales. With adjusted segment operating income increasing by 10.3% in 2019, it is very clear that their acquisitions had a direct impact on sales. This increase in adjusted segment operating income can be mainly attributed to the increased sales volume strength in project pumps and friction OEM share gains.

ITT was one of many companies across the globe that were negatively affected by the pandemic. Given their business has a heavy reliance on the travel industries, they lost out on revenue due to the decreased demand for those industries. As the automotive and airline industries see an increased usage over time again, expect the demand for ITT’s products to increase as well.

What has the stock done lately?

Over the past 3 months, the stock has generated a 18.65% return. The stock is currently trading at $72.76 and is trending towards exceeding its 52-week high of $75.56. This is great recovery from a YTD low of $35.41 that was reached in mid-March. As more positive news is released about the virus, one can assume that the stock price shall continue to rise in the near future.

Past Year Performance: ITT has returned 5.34% over the past year. This number is slightly lower than the benchmark which returned 12.85% The pandemic has had a negative effect overall on this company, but they are closing out the year back at pre-pandemic levels.

Source: Factset

My Takeaway:

ITT was originally added to the portfolio with a target price of $65.22. After recovering all of the stock price losses from the pandemic, there is reason for optimism in the near future. ITT’s strong balance sheet and willingness to expand in the past suggests that they will continue to try and increase their market share. Furthermore, as the demand for their friction brake continues to rise, so should their share price. Given these opportunities, I recommend the AIM portfolio hold ITT.

Source: Factset

Eaton Corp. Plc (NYSE: ETN, $122.74): “Must Be What They’re ETN: Why Shares Grew During the Pandemic”

By: Thomas Washington, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with any company whose stock is mentioned in this article.

Summary

· Eaton Corp. Plc (NYSE: ETN) is a diversified power management company that provides energy-efficient solutions for electrical, hydraulic, and mechanical power. ETN’s operations are segmented into Electrical Products, Electrical Systems and Services, Hydraulics, Aerospace, Vehicle and eMobility which operate within the United States and Internationally.

· Strategic direction to become an intelligent power management company through utilization of macro trends including, IoT, energy transition, electrification, and blended power.

· Target’s within planning horizon include $3B of free cashflow, 2-3% organic growth, 8-9% EPS growth, and 20% segment margins.

· In 2019 ETN launched a share buyback program to repurchase $1.9B of stock.

· ETN announced a $280M multi-year restructuring program to gain efficiencies and reduce its cost structure in response to declining market conditions.

Key Points: The $280M restructuring program includes $187M in Q2 2020 in order to reduce structural costs in markets that will have slower recovery from the pandemic. Poor market conditions brought about by the Covid-19 pandemic were the deciding factor in ETN’s decision to implement a multiyear restructuring program. Additional expected restructuring charges through 2022 are $93M including charges of $33M $55M and $5M in 2020, 2021, and 2022 respectively. The program is set to be fully implemented by 2023 at which point it is expected to yield $200M in mature year savings.

During 2019 and 2020 ETN was completed seven transactions regarding the acquisition or disposition of related companies in order to support efforts to become a more nuanced power management company. The inorganic growth strategy implemented by ETN has positioned the company nicely to enjoy growth in organic revenue in the near future. Pandemic related obstacles had a negative impact on ETN’s organic revenue, but the company managed to increase organic revenues during the year with Q3 2020 organic revenue being down 9% YTD but having increased 16% from the previous quarter.

The share repurchase program the company adopted in 2019 determined that shares were to be repurchased with market conditions, market price, and capital level all taken into account. 2020 market conditions positioned ETN nicely in order to execute 2019 program with $177M of shares being bought back in Q3 2020. Q3 repurchases brought ETN’s YTD repurchase total to $1.5B, still $400M below the programs target.

What has the stock done lately?

ETN shares have enjoyed 31.82% increase in price over the last 12 months, a very hopeful sign amid current market conditions. This level of growth in valuation is impressive no matter the year, but in the context of the last 12 months this level of growth is even more remarkable. The stock is reletavely volatile with a 52 week range of $56.41 - 120.34, but appears to be well positioned to create value in the wake of the pandemic.

Past Year Performance: ETN beat Q3 revenue forecasts by 7.5% with revenue reaching $4.5B. Earnings per share came in at $1.11, approximatly 5% above analyst predictions. Share repurchase programs indicate strong cash flow and will likely boost EPS.

Source: Factset

My Takeaway

Boasting YTD price growth of 31.82%, ETN has significiantly increased shareholder value and appears to be on track to generate returns for the next several years. The restructuring plan ETN implemented this year will give it a leg up in the post pandemic world as it will cut costs find efficiencies in the aspects of operations that were most effected by the pandemic.

Source: Factset