Azure Power Global Ltd. (AZRE, $32.02): “Up, Up, and Away”

By: Thomas Biegler, AIM Student at Marquette University

Disclosure: The AIM Equity Fund currently holds this position. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with any company whose stock is mentioned in this article.

Summary

• Azure Power Global Ltd. (NYSE: AZRE) is a holding company that engages in the development, production, and sale of solar energy.

• AZRE operates solely in India; one of the fastest growing emerging markets with an average yearly GDP growth of over 6%.

• In March 2019, Indian officials increased the country’s required solar capacity from 28 GW to 100 GW, representing a 72% increase over the three year expansion period.

• AZRE has achieved a 42% CAGR in solar capacity since their IPO in 2016 and is set to reach a minimum forward CAGR of 30% by FY 2025 through new contracted and committed projects in their portfolio.

Key points: Azure Power Global Ltd. was added to the AIM International Fund right before Covid-19 started to take its toll on US markets. At the time, the thesis behind the investment relied on three key drivers; market growth, declining costs, and long-term sustainability due to a focus on ESG. Despite the virus running rampant since then, AZRE has surpassed their own guidance and is proving their value through supporting these drivers.

AZRE’s first quarter of FY 2021 ended on June 30 and the firm showed the industry what they were made of. Over just three months, they were able to add a whopping 3,759 MW of committed power to their portfolio with 2,800 MW of capacity being fully operational by April 2021. While most of these cash flows aren’t expected to pay off until the future, the firm already experienced a 2.4% increase in revenues last quarter. Furthermore, alongside this top line growth came the value of their second driver. Even with increasing revenues, AZRE was able to cut their COGS after depreciation and amortization by a shocking 17.5% QoQ, proving that sometimes you need to spend money to make money.

In addition to expanding margins and boosting gross profit, AZRE has also remained committed to their focus towards helping the environment. To date, the company has avoided the release of over 5 million tons of CO2 and their transparency on site impact reports have helped the relatively young company gain credibility in their space. Moving forward, it can be expected that these actions will be rewarded in the form of future green bills as well as leverage on other deals that will ultimately assist in sustaining growth of cash flows to be invested.

Finally, it would not be possible to talk about AZRE without mentioning the market in which it operates. Supported by a steady Indian Rupee, India has blessed its renewable energy sector with a reduction of tariffs on production inputs of 11% plus an additional 1% over the next nine months. When added to the 50 bps reduction in interest rates, it is no wonder that this firm’s portfolio is taking off. Now with the commitment to only invest in projects with an expected return greater than the cost of capital, AZRE’s future is looking quite promising.

What has the stock done lately?

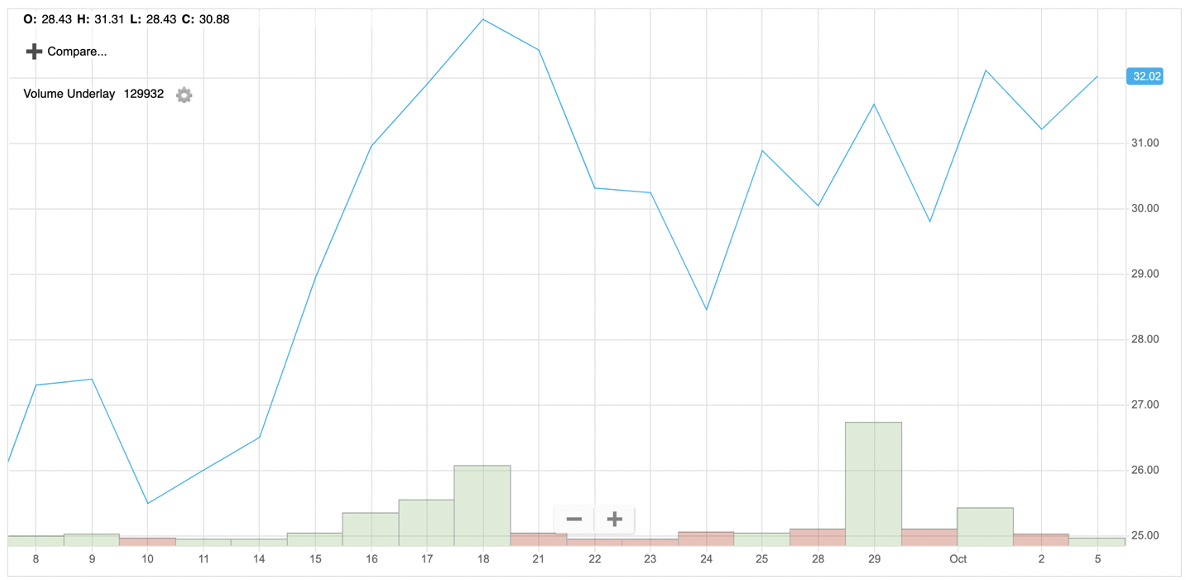

AZRE has been one of the hottest stocks in the AIM International Fund as of late. Since meetings its price target of $20.56 at the beginning of August, prices have only continued to rise surrounding heightened confidence after the firm once again crushed their earnings. Currently sitting at $32.02, AZRE is set to beat its all-time high of $32.89 which it hit mid-September.

Past Year Performance: AZRE has experienced an astounding 163% increase in share price over the last twelve months and is showing minimal signs of slowing down. With an LTM P/B value still below many peers at 2.1x and an EV/EBITDA growing alongside the industry, upside potential is still present and should be expected.

Source: FactSet

My Takeaway

AZRE has blown past its own capacity goals and is leaving its competition in the dust. Furthermore, its 45% YoY increase in operating cash flows alongside a continuously decreasing cost of production inputs will continue to allow the firm to take on bigger and better projects to generate returns. Despite already seeing a drastic rise in stock price, the certainty of capacity growth alongside the expanding renewable energy market grants AZRE a buy rating.

Source: FactSet