Takeda Pharmaceutical Co. (TAK, $14.21): “The Take on TAK”

By: Danny

Scelza, AIM Student at Marquette University

Summary

- Takeda Pharmaceutical Co. (NYSE:TAK) engages in research and development, manufacturing, and import and export of pharmaceutical products worldwide. It offers pharmaceutical products in the areas of gastroenterology, oncology, neuroscience, and rare diseases.

- Takeda is the Japanese partner for Novavax Inc’s COVID-19 vaccine and is preparing to get regulatory approval for a rollout of the vaccine early next year. As soon as the product is approved, it should be ready in time to help with Japan’s booster shot programme.

- In early September, Takeda received confirmation they have successfully addressed a warning letter from March 2020 regarding their manufacturing cite in Hikari. Takeda has upheld quality standards and thorough communication with the FDA throughout this process as the Hikari site is set to develop and manufacture 250 million Novavax doses.

- Management has indicated that they are initiating a share buyback of up to ¥100 billion, nearly $900 million, as they are looking to deliver value to their shareholders. Management believes they are buying back shares at a considerable discount and to underscore the confidence in their business

Key points:

Takeda’s diverse portfolio of 14

brands, which now represents 42% of total revenue, is the driving force in

their 13% growth in top line revenue and a 12.8% overall revenue growth and

compared to the prior year. Growth prospects from new indication and expanding

market penetration is believed by management to not be reflected in the current

share price. Their dynamic growth strategy and strong cash flow generation are

key drivers that led to the announced stock repurchase.

Within the past month, Takeda was

forced to stop their trial of TAK-994, which is an oral orexin treatment

against narcolepsy. The major setback resulted from a liver safety signal from

a patient who experienced a significant increase in liver enzymes and Takeda

discontinued the trial to protect patient safety. This discontinuation led to a

10% decrease in stock price and a 52-week low for the pharmaceutical company.

However, TAK is still developing other molecular solutions such as TAK-861 in

the same clinical area for oral orexin solutions to narcolepsy, which do not

share the same risk profile as TAK-994.

Despite the setback, management

believes their pipeline is still strong and showing increasing value,

highlighted by their Plasma-Derived therapy business. The plasma protein

therapeutics market is surging in demand, large in part to COVID-19

plasma-based insights and solutions, but also due to overall trends towards

detecting rare diseases at earlier stages. Plasma-derived therapy is a core

part of their business and they have seen promising growth trends and have

invested significant R&D expenses into this market. TAK also increased

plasma donation growth projections from 15% to 25% for 2021 to combat with

tight gross margins associated with their plasma therapies. The increase mostly

comes from high plasma donor fees, but also to support their overall target

revenue growth in that area. The Plasma-Derived therapy is anticipated to keep

growing in demand and market value through 2026 and Takeda is a large player in

that market.

What

has the stock done lately?

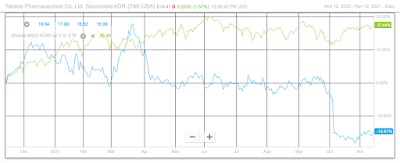

Since the TAK-994 setback, where

the stock reached a 52-week low of $13.81, the stock price currently sits at

$14.21. Setbacks in the healthcare industry can create significant headwinds

and lose investor confidence quickly and Takeda is taking necessary steps to

recover from the steep drop in share price.

Past

Year Performance:

Takeda’s 52-week price

performance is at -16.69%, again, large in part due to the TAK-994 mishap. Prior

to that, TAK was performing consistently, between a $17-$18 share price, and

the stock is sitting at a potential large discount. Management believes that

their price is discounted at 30%, hence

triggering a large share buyback. Takeda’s 2021 dividend yield is very strong

at just above 5.5%, well above the market median of 2.3%.

My

Takeaway

Sitting near the 52-week low for

TAK, the current share price makes for an interesting point of entry for

investors. Management believes TAK is severely undervalued in their current

share price as TAK has become a relatively cheap pharma business. With the

actions taken by management, of a large stock repurchase and high dividend

yields, to support their belief of undervaluation and a strategic brand growth

strategy, there is substantial reason for optimism. Not in an ideal position to

sell, the AIM fund should hold its position on TAK and anticipate share price

to bounce back.